Key Takeaways

- The best cash back cards in 2026 offer 2% flat-rate returns or up to 5% in rotating bonus categories — putting $500 to $1,000+ back in your pocket annually on typical household spending.

- Travel rewards cards can deliver 1.5 to 2.2 cents per point when redeemed through travel portals or airline/hotel transfer partners, significantly outpacing cash back on travel-heavy budgets.

- Several top cards still offer 0% introductory APR for 15 to 21 months on purchases and balance transfers, giving you an interest-free window to pay down debt or finance a large purchase.

- Annual fees range from $0 to $695. Cards with fees above $95 are only worth it if you consistently use the perks (lounge access, travel credits, statement credits) that offset the cost.

- Sign-up bonuses in 2026 range from $150 to $750+ in value, often requiring $3,000 to $6,000 in spending during the first 3 months. These bonuses can represent hundreds of dollars in first-year value.

How We Chose the Best Credit Cards

Choosing the “best” credit card is inherently personal — the right card for a frequent traveler spending $50,000 a year is very different from the right card for a college student building credit. Our methodology accounts for this by evaluating cards within specific use-case categories rather than ranking them against each other in a single list.

For each card, we analyzed six core factors:

- Reward rate and structure. We calculated the effective return on a standardized annual spending profile: $6,000 on groceries, $3,600 on gas, $2,400 on dining, $1,800 on streaming and subscriptions, $3,000 on travel, and $12,000 on everything else — roughly $28,800 in total annual spending based on Bureau of Labor Statistics consumer expenditure data.

- Sign-up bonus value. We assessed the bonus as cents-per-point using the card’s best available redemption method, then factored in the required minimum spend and time frame.

- Annual fee vs. total value. A $550 annual fee is not inherently bad if the card delivers $800+ in tangible perks. We calculated the “break-even” point for every card with a fee above $0.

- APR and financing terms. We recorded the regular purchase APR range, any introductory 0% APR offer, balance transfer terms, and penalty APR.

- Consumer protections. Purchase protection, extended warranty coverage, travel insurance, rental car coverage, and fraud liability policies were all evaluated.

- Issuer ecosystem and flexibility. We considered the breadth of transfer partners (for travel cards), the quality of the mobile app, customer service ratings from J.D. Power and the CFPB complaint database, and how easily rewards can be redeemed.

Best Credit Cards at a Glance

The following table summarizes our top picks across the most common credit card categories. Scroll down for detailed reviews of each card.

Best Cash Back Credit Cards

Cash back cards are the most straightforward way to earn rewards. You spend money, you get a percentage back — no points to decode, no transfer partners to research, no blackout dates. For the majority of consumers, a good cash back card is the single most impactful financial product they can carry in their wallet.

Citi Double Cash Card — Best Flat-Rate Cash Back

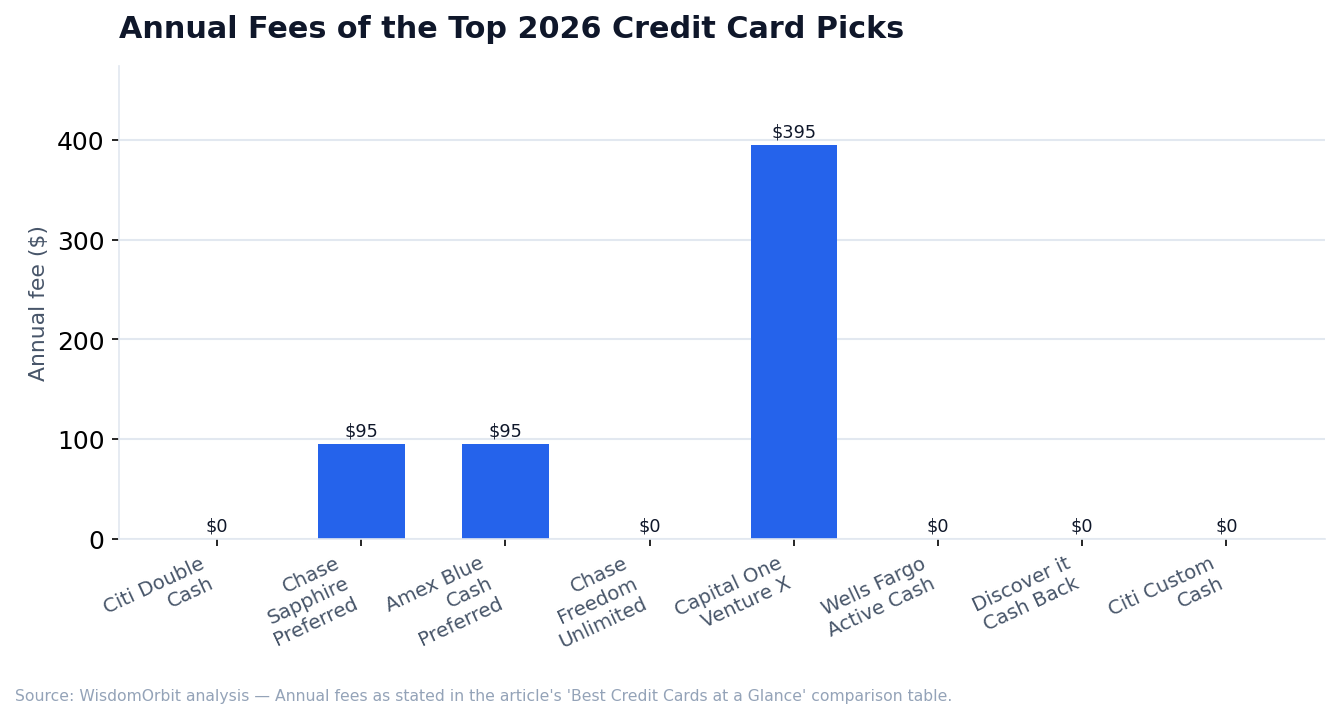

The Citi Double Cash has been the gold standard for no-fuss cash back since its launch, and it remains one of the best options in 2026. You earn 1% when you make a purchase and an additional 1% when you pay your statement, effectively giving you 2% back on every dollar spent with no annual fee and no category restrictions.

What sets the Double Cash apart from other 2% cards is its integration with Citi ThankYou points. If you also hold a Citi Premier or Citi Strata Premier card, your Double Cash rewards convert to ThankYou points that can be transferred to airline and hotel partners at ratios that often deliver 1.5 to 2 cents per point — effectively turning your 2% card into a 3%+ card for travel redemptions.

Who it is best for: Anyone who wants a simple, no-fee card that earns competitive rewards on all spending without having to think about bonus categories or activation deadlines.

Watch out for: The card has a 3% foreign transaction fee, making it a poor choice for international travel. There is also no sign-up bonus for new applicants in some periods, though Citi periodically offers a $200 bonus with $1,500 spend.

Amex Blue Cash Preferred — Best for Groceries and Families

If your household spends $500 or more per month on groceries, the Blue Cash Preferred is nearly impossible to beat. It offers 6% cash back at U.S. supermarkets (on up to $6,000 per year, then 1%), 6% on select U.S. streaming subscriptions, 3% on transit and U.S. gas stations, and 1% on everything else.

On a typical family grocery budget of $700 per month, you would earn $504 in grocery cash back alone per year. Add in $50 per month on streaming ($36 back) and $200 per month on gas ($72 back), and the card generates over $600 in annual rewards — easily justifying the $95 annual fee.

Who it is best for: Families and households with significant grocery and streaming budgets. The $95 fee is offset if you spend more than roughly $160 per month on groceries compared to using a flat 2% card.

Watch out for: The 6% rate only applies at U.S. supermarkets — wholesale clubs (Costco, Sam’s Club) and superstores (Walmart, Target) are excluded. Amex also has lower merchant acceptance than Visa and Mastercard in some areas.

Discover it Cash Back — Best for Maximizers

The Discover it Cash Back card offers 5% cash back on rotating quarterly categories (you must activate each quarter), with 1% on everything else. Categories in recent quarters have included grocery stores, restaurants, Amazon, PayPal, gas stations, and Target.

What makes Discover uniquely compelling for new cardholders is its Cashback Match program: Discover automatically matches all the cash back you earn in your first 12 months. If you earn $300 in cash back during year one, Discover gives you another $300 at the end of the year — effectively doubling your rewards to 10% in bonus categories and 2% on everything else for the first year.

Who it is best for: People who are willing to track quarterly categories and activate bonuses each quarter. Especially valuable in the first year thanks to Cashback Match.

Watch out for: The 5% categories change every quarter and require manual activation. If you forget to activate, you earn only 1%. Discover also has more limited merchant acceptance than Visa or Mastercard, particularly outside the United States.

Best Travel Rewards Credit Cards

Travel rewards cards earn points or miles that can be redeemed for flights, hotels, rental cars, and other travel expenses. The best travel cards deliver significantly more value per point than cash back cards — but they require more strategy to maximize. The key is understanding transfer partners and redemption sweet spots.

Chase Sapphire Preferred — Best Mid-Tier Travel Card

The Chase Sapphire Preferred is the most popular travel rewards card in the United States, and for good reason. It earns 3x points on dining (including takeout and eligible delivery services), 3x on online grocery purchases (excluding Target, Walmart, and wholesale clubs), 2x on all travel, and 1x on everything else. Points are worth 25% more when redeemed through Chase Travel, giving them an effective value of 1.25 cents each.

But the real value lies in Chase’s transfer partner network. Chase Ultimate Rewards points transfer 1:1 to 14 airline and hotel partners, including United, Southwest, Hyatt, and Marriott. A savvy traveler can regularly get 1.5 to 2.2 cents per point through partner transfers — meaning those 3x dining points are effectively earning 4.5% to 6.6% back on every restaurant meal.

The sign-up bonus of 75,000 points (after spending $5,000 in the first 3 months) is worth at least $937 through Chase Travel and potentially more through transfer partners. That alone more than justifies the $95 annual fee for the first year.

Who it is best for: Travelers who dine out frequently and want the flexibility of transferable points without paying a premium annual fee. This card is also an excellent entry point into the Chase ecosystem.

Watch out for: The $95 annual fee is not waived the first year. Also, if you never use the transfer partners and always redeem for cash back (at 1 cent per point), you are better off with a flat 2% card.

Capital One Venture X — Best Premium Travel Card

The Capital One Venture X has disrupted the premium card market by offering nearly all the perks of the Amex Platinum and Chase Sapphire Reserve at a significantly lower effective cost. The card earns 2x miles on every purchase, 10x on hotels and rental cars booked through Capital One Travel, and 5x on flights booked through Capital One Travel.

The $395 annual fee sounds steep, but the card includes a $300 annual travel credit (automatically applied to Capital One Travel bookings) and 10,000 bonus miles on each account anniversary (worth $100). That brings the effective annual fee down to just $0 — before you even factor in the other perks.

Those perks include unlimited Priority Pass lounge access (including restaurants), a Capital One Lounge network that is actively expanding, Global Entry or TSA PreCheck credit ($100 every 4 years), trip cancellation and interruption insurance, primary rental car coverage, and no foreign transaction fees.

Capital One miles transfer 1:1 to 15+ airline and hotel partners, including Air Canada Aeroplan, Turkish Miles & Smiles, Wyndham, and Accor. Valuations through transfer partners regularly exceed 1.5 cents per mile.

Who it is best for: Frequent travelers who want premium perks and lounge access without a net-positive annual fee. Especially strong for international travelers due to no foreign transaction fees and excellent transfer partners.

Watch out for: The $300 travel credit only applies to bookings through Capital One Travel, which does not always have the lowest prices. The 10x and 5x earning rates also only apply to Capital One Travel bookings.

Best 0% APR and Balance Transfer Cards

If you are carrying high-interest credit card debt or planning a large purchase you need time to pay off, a 0% introductory APR card can save you hundreds or even thousands of dollars in interest. The key is choosing a card with a long promotional period and a reasonable balance transfer fee.

Wells Fargo Active Cash — Best 0% APR + Rewards Combo

The Wells Fargo Active Cash card combines a flat 2% cash back rate on all purchases with a 0% introductory APR for 15 months on both purchases and qualifying balance transfers. This makes it one of the rare cards that excels at both earning rewards and providing interest-free financing.

After the promotional period, the variable APR ranges from 20.24% to 29.24% based on your creditworthiness. The balance transfer fee is 3% for the first 120 days ($5 minimum), then 5% thereafter.

For someone transferring a $5,000 balance from a card charging 24% APR, the Active Cash would save approximately $1,200 in interest over the 15-month promotional period (minus the $150 balance transfer fee), for a net savings of $1,050.

Who it is best for: People who want to consolidate existing credit card debt while also earning strong rewards on new purchases. The 2% flat rate means you do not sacrifice rewards for the 0% APR benefit.

Citi Custom Cash — Best for Single-Category Maximizers

The Citi Custom Cash automatically identifies your highest-spending category each billing cycle and gives you 5% back on that category (up to $500 in spending per cycle), plus 1% on everything else. Eligible categories include restaurants, gas stations, grocery stores, select travel, select transit, select streaming, drugstores, home improvement stores, fitness clubs, and live entertainment.

The card also offers a 0% introductory APR for 15 months on purchases and balance transfers. Combined with the automatic 5% earning on your top category, this card delivers excellent first-year value.

The math works out well for focused spenders. If your top category is dining and you spend $500 per month at restaurants, you earn $25 per month (5%) on dining alone — $300 per year from a single category on a no-annual-fee card.

Who it is best for: People with one dominant spending category who do not want to manage rotating category activations. Pairs extremely well with a flat 2% card for non-category spending.

How Credit Card Rewards Actually Work

Before choosing a card, it helps to understand the three main reward structures and how issuers fund them.

Cash back is the simplest model. You earn a percentage of each purchase as a statement credit, direct deposit, or check. One cent of cash back equals one cent of value, always. There is no ambiguity.

Points (Chase Ultimate Rewards, Amex Membership Rewards, Citi ThankYou Points, Capital One Miles) are more flexible but more complex. One point can be worth anywhere from 0.5 cents to 3+ cents depending on how you redeem it. Redeeming for gift cards or merchandise typically delivers the worst value (0.5 to 0.8 cents per point). Redeeming for travel through the issuer’s portal delivers moderate value (1.0 to 1.5 cents). Transferring to airline and hotel partners can deliver the highest value (1.5 to 2.5+ cents), but requires research and flexibility.

Airline and hotel co-branded points (Delta SkyMiles, United MileagePlus, Marriott Bonvoy, Hilton Honors) can only be used within that brand’s ecosystem. They often offer higher earning rates on purchases within the brand but provide less flexibility overall.

Card issuers fund rewards primarily through interchange fees — the 1.5% to 3.5% fee that merchants pay to accept credit cards. Premium cards with higher rewards tend to carry higher interchange fees, which is why some small businesses prefer customers use debit cards or cash.

Credit Card Interest Rates in 2026: What You Need to Know

The average credit card APR in early 2026 is approximately 21.5%, according to Federal Reserve data. This is near the highest levels in decades, driven by the elevated federal funds rate that has remained in the 4.25% to 4.50% target range.

Credit card APRs are calculated as the prime rate (currently 7.50%) plus a margin set by the issuer (typically 12% to 22%). Your individual APR depends on your credit score, income, existing debt load, and the issuer’s underwriting criteria.

Here is why this matters for card selection: if you carry a balance month to month, interest charges will almost certainly wipe out any rewards you earn. A cardholder with a $5,000 revolving balance at 21.5% APR pays roughly $1,075 per year in interest. Even the best rewards card earning 2% on $28,800 in annual spending only generates $576 in rewards. The interest cost is nearly double the reward value.

The bottom line: rewards cards are only a good deal if you pay your statement balance in full every month. If you are currently carrying a balance, prioritize a 0% APR balance transfer card to eliminate interest, then switch to a rewards card once you are debt-free.

How to Choose the Right Credit Card for You

With dozens of competitive options on the market, narrowing down the right card requires honest self-assessment. Here is a decision framework based on the three questions that matter most:

Step 1: Do You Carry a Balance?

If you carry a credit card balance from month to month, stop chasing rewards. Your priority should be a 0% introductory APR card (like the Wells Fargo Active Cash or Citi Custom Cash) or a dedicated balance transfer card. Pay off your existing debt during the promotional period, then graduate to a rewards card once you can pay in full every month.

Step 2: What Are Your Top Spending Categories?

Review your last three months of credit card and bank statements. Categorize your spending into groceries, dining, gas, travel, subscriptions, and general purchases. If one category dominates (say, $600+ per month on groceries), a category-bonus card will outperform a flat-rate card. If your spending is evenly distributed, a flat 2% card is almost certainly your best bet.

Step 3: Are You Willing to Manage Complexity?

The highest-value strategy in credit cards involves carrying 2-3 cards and routing each purchase to the card with the best bonus for that category. For example: Amex Blue Cash Preferred for groceries and streaming, Chase Sapphire Preferred for dining and travel, and a Citi Double Cash for everything else. This “trifecta” approach can yield 3% to 6% effective returns across all spending — but it requires organizational effort.

If you want one card in your wallet and no mental overhead, a 2% flat-rate card (Citi Double Cash or Wells Fargo Active Cash) is the pragmatic choice. You will leave some value on the table compared to a multi-card strategy, but you will never forget which card to use or miss a category activation deadline.

Credit Card Fees Explained

Understanding the full fee structure is essential before committing to any card. Here are the fees you may encounter:

- Annual fee ($0 to $695): Charged once per year for card membership. Cards with annual fees must deliver enough value in rewards, credits, and perks to justify the cost. As a rule of thumb, a card is worth its annual fee if its total annual value (rewards + credits + perks you actually use) exceeds the fee by at least 50%.

- Foreign transaction fee (0% to 3%): Charged on purchases made in a foreign currency or processed by a foreign bank. Most travel cards waive this fee. If you travel internationally even once a year, make sure your card has no foreign transaction fee.

- Balance transfer fee (3% to 5%): A one-time fee charged when you transfer a balance from another card. On a $5,000 transfer, a 3% fee costs $150. Factor this into your savings calculation when evaluating 0% APR offers.

- Cash advance fee (3% to 5%): Charged when you use your card to withdraw cash from an ATM. Cash advances also begin accruing interest immediately with no grace period and often at a higher APR than purchases. Avoid cash advances entirely.

- Late payment fee (up to $41): Charged when you miss the minimum payment due date. Late payments can also trigger a penalty APR (up to 29.99%) and will be reported to credit bureaus if the payment is more than 30 days late, damaging your credit score.

Building Credit with Your First Card

If you have no credit history or a limited credit file, your path into the credit card world typically starts with one of two products: a secured credit card or a student credit card.

A secured credit card requires a refundable security deposit (typically $200 to $500) that serves as your credit limit. You use the card like any other credit card, and your payment history is reported to all three major credit bureaus (Equifax, Experian, TransUnion). After 6 to 12 months of responsible use, most issuers will refund your deposit and upgrade you to an unsecured card with a higher limit.

The Discover it Secured card is the standout choice in this category because it earns 2% cash back at gas stations and restaurants (on up to $1,000 in combined purchases each quarter) and 1% on everything else — plus the Cashback Match in year one. Most secured cards offer zero rewards, so this is a significant differentiator.

A student credit card is designed for college students with limited income and credit history. These cards have lower credit limits and fewer perks, but they do not require a security deposit. The Discover it Student Cash Back card mirrors the earning structure of the regular Discover it card (5% rotating categories + Cashback Match) and is one of the best student cards available.

Whichever route you take, the three rules for building credit are simple: (1) always pay at least the minimum on time, (2) keep your utilization below 30% of your credit limit, and (3) do not open multiple new accounts in a short period.

Common Credit Card Mistakes to Avoid

After years of reviewing credit cards and talking to thousands of readers, these are the most costly mistakes I see people make:

- Spending more to earn rewards. This is the single most common trap. Earning 2% cash back on a $200 impulse purchase “saves” you $4 but costs you $200. Rewards should be a byproduct of spending you would do anyway, never a motivation to spend more.

- Paying only the minimum. On a $5,000 balance at 21.5% APR, making only the minimum payment would take over 16 years to pay off and cost more than $6,800 in interest — more than the original balance. Always pay as much as you can above the minimum.

- Ignoring the sign-up bonus requirements. Many people apply for a card with a $750 sign-up bonus but fail to meet the $4,000 spending requirement within the 3-month window. Read the terms before applying and plan your spending accordingly.

- Closing old cards. Closing a credit card reduces your total available credit (increasing your utilization ratio) and can shorten your average age of accounts — both of which hurt your credit score. If a card has no annual fee, keep it open even if you rarely use it.

- Carrying a balance to “build credit.” This is a persistent myth. You do not need to carry a balance or pay interest to build credit. Paying your statement in full every month builds credit just as effectively while costing you nothing in interest.

Frequently Asked Questions

What credit score do I need to get approved for a rewards credit card?

Most premium rewards credit cards require a good to excellent credit score, typically 670 or higher on the FICO scale. Top-tier travel cards like the Chase Sapphire Reserve or Amex Platinum generally require scores of 720 or above. However, several solid cash back cards are available to applicants with fair credit (580–669), including secured credit cards that can help you build credit over time. Your income, existing debt, and recent credit inquiries also factor into approval decisions.

Is it better to get a cash back card or a travel rewards card?

It depends on your spending habits and lifestyle. Cash back cards are simpler and better for people who want straightforward savings without managing points. Travel rewards cards offer higher potential value per point (often 1.5 to 2 cents per point when redeemed for travel) but require more effort to maximize. If you spend more than $3,000 per year on travel, a travel card will likely deliver more value. If you prefer simplicity, cash back is the better choice. Many experienced cardholders use both: a cash back card for everyday spending and a travel card for dining and trip-related purchases.

How many credit cards should I have?

There is no single right answer. The average American has 3 to 4 credit cards. Having multiple cards can help your credit score by lowering your overall credit utilization ratio, but only if you manage them responsibly. A common strategy is to have one flat-rate cash back card for everyday spending and one category-bonus card for your highest expense categories. Opening too many cards in a short period can temporarily lower your score due to hard inquiries. Wait at least 3 to 6 months between new applications.

Do 0% APR offers affect my credit score?

Applying for a 0% APR card will trigger a hard inquiry on your credit report, which may temporarily lower your score by 5 to 10 points. However, using the card responsibly can improve your score over time by adding to your available credit and building a positive payment history. The 0% introductory period itself does not directly affect your score. What matters is making at least the minimum payment on time every month and keeping your utilization below 30%.

What happens when a 0% APR promotional period ends?

When the promotional period ends, any remaining balance will begin accruing interest at the card’s regular variable APR, which typically ranges from 18.99% to 29.99% in 2026. Unlike deferred-interest retail store cards, most bank-issued 0% APR cards do not retroactively charge interest on balances you already paid off during the promotional period. You should aim to pay off the entire balance before the promotion expires to avoid interest charges entirely. Set up automatic payments or divide your balance by the number of remaining promotional months to create a payoff plan.

Editor’s Insight

The most important principle in choosing a card is this: the best credit card is the one that matches your actual behavior, not your aspirational behavior. If you eat out twice a month, a card that earns 4x on dining is wasted on you. If you have never transferred points to an airline partner, a premium travel card’s transfer network has zero practical value. Be honest about how you spend and how much effort you are willing to invest in optimization. For most people, a no-annual-fee 2% cash back card and one category-bonus card for their top spending area will capture 80% of the value with 20% of the complexity. Leave the spreadsheet optimization to the hobbyists.

Sources & References

- Federal Reserve. “Consumer Credit — G.19 Report.” federalreserve.gov

- Consumer Financial Protection Bureau (CFPB). “The Consumer Credit Card Market Report.” consumerfinance.gov

- Bureau of Labor Statistics. “Consumer Expenditures — 2024.” bls.gov

- J.D. Power. “2025 U.S. Credit Card Satisfaction Study.” jdpower.com

- Federal Reserve Bank of New York. “Quarterly Report on Household Debt and Credit.” newyorkfed.org

- FICO. “What Is a Good Credit Score?” myfico.com