Invoice factoring lets you sell your unpaid invoices to a factoring company for immediate cash. Instead of waiting 30, 60, or 90 days for customers to pay, you get most of the money upfront - typically within 24 to 48 hours. This powerful financing tool has helped countless B2B businesses bridge cash flow gaps and fuel growth without taking on traditional debt.

For businesses that invoice other companies, slow payment cycles can create serious cash flow problems. You've delivered the product or service, but you can't pay your suppliers, employees, or overhead until your customer pays their invoice. Invoice factoring solves this problem by converting your accounts receivable into working capital on demand.

How Invoice Factoring Works

The invoice factoring process is straightforward, though it's important to understand each step to maximize its benefits for your business:

- Invoice your customer - Complete your work and send an invoice as you normally would, with net-30, net-60, or net-90 payment terms

- Submit invoice to factor - Send the invoice to your factoring company through their portal or email

- Verification - The factor verifies the invoice is legitimate and the customer has good credit

- Receive advance - Get 80-95% of the invoice value deposited to your account, often within 24 hours

- Factor collects payment - The factoring company collects payment directly from your customer when the invoice is due

- Receive reserve - Once your customer pays, you receive the remaining balance minus the factoring fee

Types of Invoice Factoring

Recourse Factoring

With recourse factoring, you're responsible if your customer doesn't pay. If the invoice goes unpaid after a certain period (typically 60-90 days), you must buy it back from the factor. Recourse factoring is more common and has lower fees because the factoring company carries less risk.

Non-Recourse Factoring

Non-recourse factoring transfers the credit risk to the factoring company. If your customer goes bankrupt or simply refuses to pay, you're not on the hook. However, non-recourse factoring comes with higher fees and stricter requirements about which invoices qualify.

Spot Factoring

Spot factoring lets you factor individual invoices as needed rather than committing to a long-term contract. This flexibility is ideal for businesses that only occasionally need cash flow help, though per-invoice rates are typically higher.

Contract Factoring

Contract factoring involves an ongoing relationship where you factor all or most of your invoices over time. Volume commitments often result in lower rates, and the factor becomes familiar with your customers and business patterns.

Top Invoice Factoring Companies

BlueVine

BlueVine offers invoice factoring up to $5 million with advances up to 90% of invoice value. Their online platform makes it easy to submit invoices and track payments. BlueVine is known for fast approvals (often same-day) and competitive rates starting at 0.25% per week. They work with a wide range of industries and don't require long-term contracts.

Fundbox

Fundbox provides invoice financing (rather than true factoring) up to $150,000, meaning you still collect payment from customers. Their standout feature is the simple credit draw model - connect your accounting software, and they'll extend credit based on your outstanding invoices. Rates start at 4.66% for 12-week terms.

AltLINE

AltLINE by Southern Bank specializes in factoring for specific industries including staffing, trucking, manufacturing, and government contractors. They offer both recourse and non-recourse options with advance rates up to 90%. As a bank-owned factor, they can offer more competitive rates than independent factoring companies.

Triumph Business Capital

Triumph is the leading factoring company for the trucking and freight industry, factoring over $3 billion in invoices annually. They offer fuel advances, same-day funding, and a robust mobile app for truckers. If you're in transportation, Triumph's industry expertise and carrier-specific features make them a top choice.

RTS Financial

RTS Financial focuses exclusively on transportation and logistics businesses, offering factoring, fuel discount programs, and back-office support. They provide same-day funding on approved loads and have factored billions in freight invoices. Their industry focus means they understand the unique challenges of transportation businesses.

Invoice Factoring Costs

Understanding factoring costs helps you evaluate whether the cash flow benefits outweigh the expense:

- Factor rate - The primary cost, typically 1% to 5% of the invoice value. Rates vary based on invoice volume, customer creditworthiness, and industry risk.

- Advance rate - The percentage you receive upfront, usually 80% to 95%. Higher advances mean more immediate cash but sometimes higher fees.

- Reserve holdback - The portion held until your customer pays (5-20%), returned to you minus fees after collection.

- Additional fees - Watch for wire transfer fees ($15-30), monthly minimum fees, account setup fees, and credit check fees.

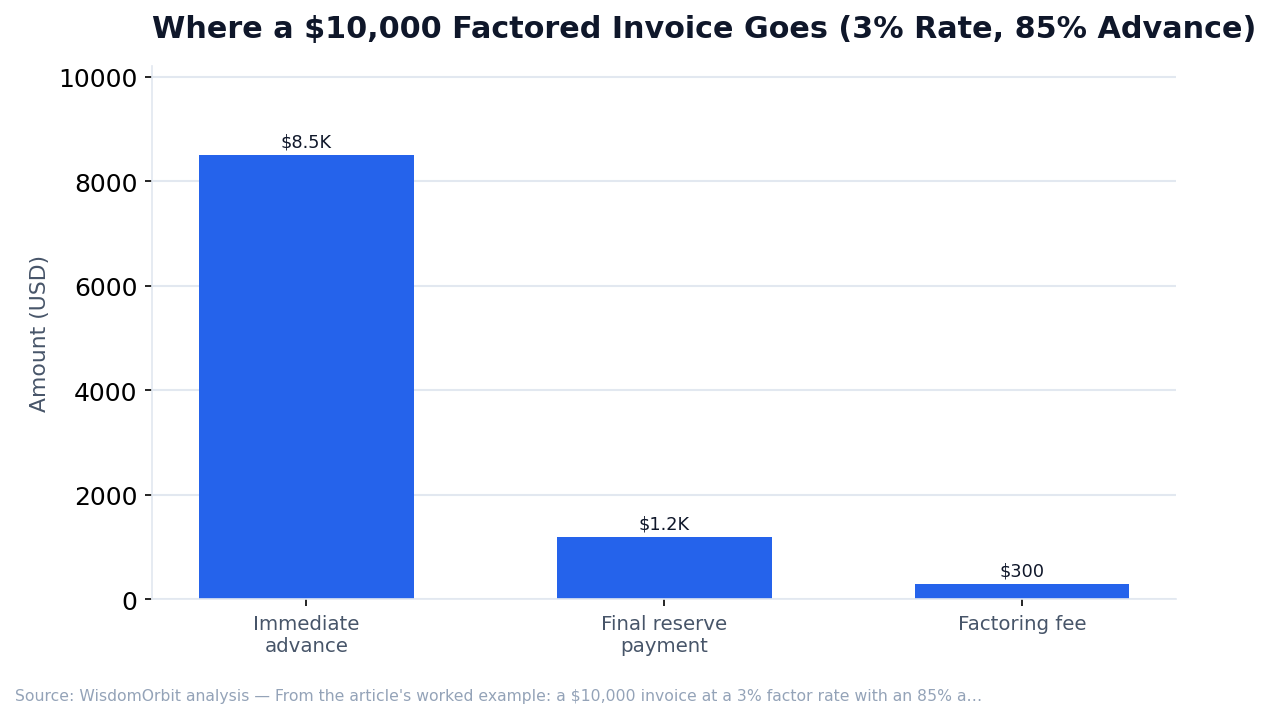

Example Cost Calculation

You factor a $10,000 invoice with a 3% factor rate and 85% advance:

- Immediate advance: $8,500 (85% of $10,000)

- Reserve held: $1,500 (15% of $10,000)

- Factoring fee: $300 (3% of $10,000)

- Final reserve payment: $1,200 ($1,500 minus $300 fee)

- Total received: $9,700

Factoring vs Invoice Financing

These terms are often confused, but they work differently:

- Invoice Factoring - You sell your invoices to the factor, who then collects payment directly from your customers. Your customers know you're using a factor because they pay the factoring company.

- Invoice Financing - You borrow money using invoices as collateral but still collect payment from customers yourself. This keeps the financing relationship private but means you handle collections.

Choose factoring if you want to outsource collections. Choose financing if keeping customer relationships private is important to your business.

Industries That Benefit Most

While any B2B business can use factoring, certain industries rely on it heavily:

- Trucking and Transportation - Long payment cycles and high fuel costs make factoring essential

- Staffing Agencies - Pay employees weekly but invoice clients monthly

- Manufacturing - Large orders require cash for materials before payment arrives

- Wholesale and Distribution - High-volume, low-margin businesses need fast cash cycles

- Government Contractors - Government agencies are reliable but slow to pay

- Construction - Project-based payment schedules create cash flow gaps

Pros and Cons of Invoice Factoring

Advantages

- Fast access to cash - Funding within 24-48 hours vs. 30-90 days

- No debt on your books - Factoring is a sale, not a loan

- Easier qualification - Approval based on customer credit, not yours

- Scales with growth - Factor more invoices as revenue increases

- Outsourced collections - Factor handles payment follow-up

Disadvantages

- Cost - More expensive than traditional bank loans

- Customer relationships - Customers know you're using a factor

- Dependency - Can become a crutch if cash flow problems aren't addressed

- Contract requirements - Some factors require volume minimums or long-term contracts

Frequently Asked Questions

Will factoring hurt my customer relationships?

Most customers are familiar with factoring, especially in industries like trucking and staffing where it's common. Professional factors handle collections diplomatically. However, if discretion is crucial, invoice financing might be a better choice.

Can startups use invoice factoring?

Yes, because approval is based on your customers' credit rather than your business history. Even new businesses can qualify if they invoice creditworthy B2B customers.

What happens if my customer doesn't pay?

With recourse factoring, you're responsible for buying back the unpaid invoice. With non-recourse factoring, the factor absorbs the loss (but only for qualifying invoices and situations like customer bankruptcy).

How long does approval take?

Initial approval typically takes 3-7 days as the factor verifies your business and customers. After setup, individual invoices can be funded within 24 hours.

Can I factor invoices from all my customers?

Factors evaluate each customer individually. Customers with poor credit or payment history may not qualify, and factors typically won't purchase invoices from consumers (B2C businesses).

Choosing the Right Factoring Company

Consider these factors when selecting a factoring partner:

- Industry experience - Factors specializing in your industry understand your business better

- Rate structure - Compare total costs, not just the headline rate

- Contract flexibility - Look for spot factoring or no long-term commitment if you want flexibility

- Advance percentage - Higher advances improve cash flow but may come with higher fees

- Funding speed - Confirm same-day or next-day funding is available

- Customer service - Your customers will interact with the factor, so professionalism matters

You May Also Like

Sources & References

- International Factoring Association – Industry Statistics and Standards

- Commercial Finance Association – Asset-based lending and factoring data

- U.S. Small Business Administration – Alternative financing resources

- Federal Reserve – Business credit and receivables financing data

Related Articles

This article is for general information only and is not financial, legal, or tax advice. Verify current rates, fees, and terms with providers before making decisions.