Key Takeaways

- Term life insurance is the most affordable way to protect your family

- Buy coverage equal to 10-15x your annual income as a starting point

- Lock in rates while young and healthy; premiums increase significantly with age

Life insurance provides financial protection for your loved ones if something happens to you. A death benefit payment can cover funeral costs, replace lost income, pay off debts, fund children's education, and ensure your family maintains their standard of living during an incredibly difficult time. Life insurance isn't about you - it's about protecting the people who depend on you financially.

Over 100 million Americans lack adequate life insurance, often because they overestimate costs or don't understand their options. Term life insurance for a healthy 30-year-old can cost less than a streaming subscription while providing hundreds of thousands in protection. Understanding your options helps you make the right choice for your family's security.

Types of Life Insurance

Term Life Insurance

Coverage for a specific period - typically 10, 20, or 30 years. Term life is the most affordable option because it provides pure death benefit protection without cash value. If you die during the term, your beneficiaries receive the full death benefit. If you outlive the term, coverage ends unless you renew (at much higher rates) or convert to permanent insurance.

Term life is ideal for covering specific time-limited obligations: paying off a mortgage, replacing income while children are young, covering a spouse until retirement. Most financial experts recommend term life for the majority of people because of its simplicity and value.

Whole Life Insurance

Permanent coverage that lasts your entire life, as long as premiums are paid. Whole life includes a cash value component that grows at a guaranteed rate over time. You can borrow against the cash value or surrender the policy for its cash value. Premiums are fixed and higher than term life, but never increase.

Whole life works well for estate planning, leaving a guaranteed inheritance, or covering final expenses. The forced savings aspect appeals to some, though many financial advisors suggest buying term and investing the difference for better returns.

Universal Life Insurance

Flexible permanent coverage with adjustable premiums and death benefits. Cash value earns interest based on current market rates. You can increase or decrease premiums and death benefits as your needs change, subject to policy limits. More complex than whole life but offers more customization.

Variable Life Insurance

Permanent insurance where cash value is invested in sub-accounts similar to mutual funds. Higher potential returns but also more risk - cash value can decrease if investments perform poorly. Requires active management decisions.

Indexed Universal Life (IUL)

Cash value growth tied to a stock market index (like the S&P 500) with downside protection. Offers potential for higher returns than traditional universal life while limiting losses. Popular but complex with fees that can erode value.

Final Expense Insurance

Simplified whole life policies designed to cover burial costs and end-of-life expenses, typically $5,000-$25,000 coverage. Easier qualification with less health screening. Premium for those who can't qualify for larger policies.

Top Life Insurance Companies

Haven Life

Best for online term life applications. Backed by MassMutual, Haven offers a streamlined digital experience with instant decisions for many applicants. Competitive rates and no medical exam for qualifying applicants under certain coverage amounts.

Northwestern Mutual

Best for whole life and permanent policies. The largest direct provider of individual life insurance in the US, known for financial strength and dividend payments to policyholders. Works through financial advisors for personalized planning.

State Farm

Best for bundling with auto and home insurance. Extensive local agent network provides face-to-face service. Competitive rates and discounts when combining multiple policies.

Prudential

Best for no-exam policies. Offers simplified issue policies up to $1 million for qualifying applicants. Strong financial ratings and diverse product options from term to complex permanent insurance.

MassMutual

Best for dividend-paying whole life. As a mutual company, MassMutual is owned by policyholders and has paid dividends every year since 1869. Strong financial ratings and comprehensive permanent insurance options.

Ladder

Best for flexible term coverage. Allows you to adjust coverage amounts as your needs change without applying for a new policy. Entirely online application with instant decisions available.

USAA

Best for military members and families. Excellent rates and service for those who qualify (military members, veterans, and their families). Consistently high customer satisfaction ratings.

How Much Life Insurance Do You Need?

The right amount depends on your financial obligations and family situation. Common calculation methods:

10x Income Rule

Multiply your annual income by 10 for a quick estimate. Simple but doesn't account for your specific debts, expenses, or existing savings.

DIME Formula

A more comprehensive approach that calculates:

- Debt - Total outstanding debts (credit cards, student loans, car loans)

- Income - Years of income to replace multiplied by annual salary

- Mortgage - Remaining mortgage balance

- Education - Expected college costs for children

Add these together and subtract existing life insurance and savings to find your coverage gap.

Human Life Value

Calculates the present value of your future earning potential based on your age, occupation, projected career earnings, and benefits. More precise but requires detailed analysis.

Consider These Factors

- Would your spouse/partner need to work or work more?

- Would your family need to relocate or downsize?

- Do you have children who need care or education funding?

- Do you have debts that would burden your family?

- What existing savings, investments, or employer life insurance do you have?

Average Life Insurance Costs

Premiums vary significantly based on age, health, smoking status, and coverage amount:

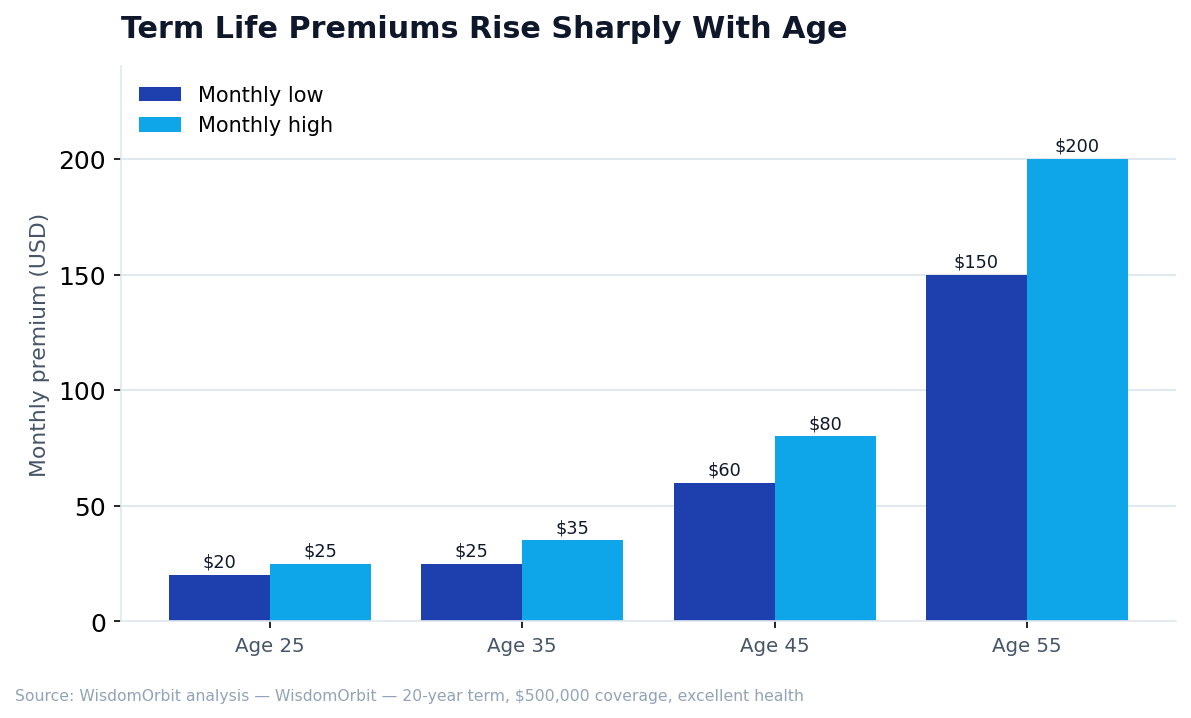

Term Life (20-Year, $500,000 Coverage)

- Age 25, Excellent Health - $20-25/month

- Age 35, Excellent Health - $25-35/month

- Age 45, Excellent Health - $60-80/month

- Age 55, Excellent Health - $150-200/month

- Smoker - 2-3x higher than non-smoker rates

Whole Life ($250,000 Coverage)

- Age 30 - $200-250/month

- Age 40 - $300-350/month

- Age 50 - $450-550/month

Factors That Affect Rates

- Age - Younger is always cheaper. Lock in rates early.

- Health - Medical conditions, weight, and family history impact rates

- Tobacco Use - Smokers pay 2-4x more than non-smokers

- Coverage Amount - Higher coverage costs more, but rate per $1,000 often decreases

- Term Length - Longer terms cost more annually

- Occupation/Hobbies - High-risk jobs or activities increase premiums

The Application Process

- Get Quotes - Compare rates from multiple companies online

- Apply - Complete application with health and lifestyle questions

- Medical Exam - Many policies require a health exam (blood, urine, measurements). No-exam policies cost more but offer convenience.

- Underwriting - Company reviews your application and medical records

- Approval - Receive offer with your rate classification

- Policy Delivery - Review policy, make first premium payment, coverage begins

Frequently Asked Questions

Do I need life insurance if I'm single?

Maybe. Consider if anyone would be burdened by your debts, if you want to leave money to family or charity, or if you want to lock in low rates while young and healthy.

How long does approval take?

Traditional policies with medical exams take 4-8 weeks. No-exam policies can provide instant decisions or approval within days.

Can I get life insurance with health conditions?

Yes, though rates will be higher. Many conditions that were once uninsurable can now be covered. Work with an independent agent who can shop multiple carriers for the best rate.

What happens if I miss a payment?

Most policies have a 30-day grace period. After that, the policy may lapse. Some permanent policies allow using cash value to cover premiums temporarily.

Getting Started

Start by calculating how much coverage you need, then compare quotes from multiple companies. Consider working with an independent insurance agent who can shop multiple carriers. Apply while you're healthy - waiting until you need insurance often means you can't get it or will pay much more.

Editor's Insight

The life insurance industry loves to complicate things, but here's the truth: most people under 50 with dependents need a 20-year term policy for 10-12x their annual income. That's it. A healthy 35-year-old can get $500,000 in coverage for under $30/month.

Whole life and universal life policies have their place, but they're often oversold to people who would be better served by cheap term insurance plus investing the difference. Don't let anyone convince you that life insurance is an "investment" — it's protection for your family, period.

Sources & References

- LIMRA – 2024 Insurance Barometer Study – Reports that 42% of Americans say they need more life insurance coverage

- National Association of Insurance Commissioners (NAIC) – Life insurance buyer's guides and company complaint data

- American Council of Life Insurers (ACLI) – Industry Facts – Life insurance ownership statistics

- Insurance Information Institute – Life insurance basics and policy type explanations

- Society of Actuaries – Mortality tables and life expectancy data used in premium calculations