Key Takeaways

- Home equity loan rates in early 2026 range from about 7.49% to 10.50% APR for well-qualified borrowers, depending on the lender, LTV ratio, and loan term.

- Most lenders require a combined loan-to-value (CLTV) ratio of 80% to 85%, though some (like Navy Federal) go up to 100%.

- A fixed rate and lump-sum payout make home equity loans ideal for large, one-time expenses such as renovations, debt consolidation, or major purchases.

- Interest may be tax-deductible if you use the proceeds to buy, build, or substantially improve the home securing the loan (IRS Publication 936).

- On a $50,000 home equity loan at 8.25% over 15 years, you would pay approximately $36,400 in total interest — making rate shopping essential.

What Is a Home Equity Loan?

A home equity loan is a second mortgage that lets you borrow a lump sum against the equity you have built in your home. Equity is the difference between your home's current appraised value and the outstanding balance on your primary mortgage. If your home is worth $400,000 and you owe $250,000 on your mortgage, you have $150,000 in equity.

Unlike a home equity line of credit (HELOC), which works like a revolving credit card, a home equity loan delivers the full amount upfront and charges a fixed interest rate. You repay the loan in equal monthly installments over a set term — typically 5, 10, 15, 20, or 30 years. Because the loan is secured by your property, lenders can offer rates significantly lower than unsecured personal loans or credit cards.

The trade-off is risk: if you fail to repay, the lender can foreclose on your home. That makes it essential to borrow only what you need and to ensure the monthly payment fits comfortably within your budget.

How Home Equity Loans Work: The Mechanics

Understanding the math behind home equity loans is critical before you apply. The two most important numbers are your loan-to-value ratio (LTV) and your combined loan-to-value ratio (CLTV).

Loan-to-Value (LTV) and Combined LTV (CLTV)

Your LTV on your primary mortgage is calculated by dividing your mortgage balance by your home's appraised value. Your CLTV adds the proposed home equity loan to the equation:

Example: Your home appraises at $400,000. You owe $250,000 on your mortgage and want a $50,000 home equity loan.

- Primary LTV: $250,000 ÷ $400,000 = 62.5%

- CLTV: ($250,000 + $50,000) ÷ $400,000 = 75%

At 75% CLTV, you would qualify with most lenders (who typically cap CLTV at 80–85%). The lower your CLTV, the better rate you will generally receive.

How Much Can You Borrow?

Most lenders allow you to borrow up to 80% of your home's value minus your existing mortgage balance. Some go higher:

The 2026 Home Equity Loan Rate Landscape

Home equity loan rates are influenced by the Federal Reserve's benchmark rate, the 10-year Treasury yield, and lender-specific pricing. As of early 2026, the federal funds rate stands at 4.25%–4.50% after the Fed's measured easing cycle that began in late 2024.

For home equity loans specifically, average fixed rates in early 2026 range from approximately 8.00% to 10.00% APR for borrowers with good credit (680+), and as low as 7.49% to 8.50% for excellent credit (740+) at the most competitive lenders. These rates are notably higher than primary mortgage rates (which hover near 6.5%–7.0%) because home equity loans represent a second lien — meaning the lender gets paid after the primary mortgage holder in a foreclosure.

The key factors that affect your personal rate include:

- Credit score: Each 20-point increase above 680 can shave 0.25–0.50% off your rate.

- CLTV ratio: Lower CLTV = lower rate. Borrowing 60% CLTV will price significantly better than 85%.

- Loan term: Shorter terms (5–10 years) often carry lower rates than 20–30 year terms.

- Loan amount: Some lenders offer better pricing on loans above $25,000 or $50,000.

- Property type: Primary residences qualify for the best rates; investment properties pay a premium.

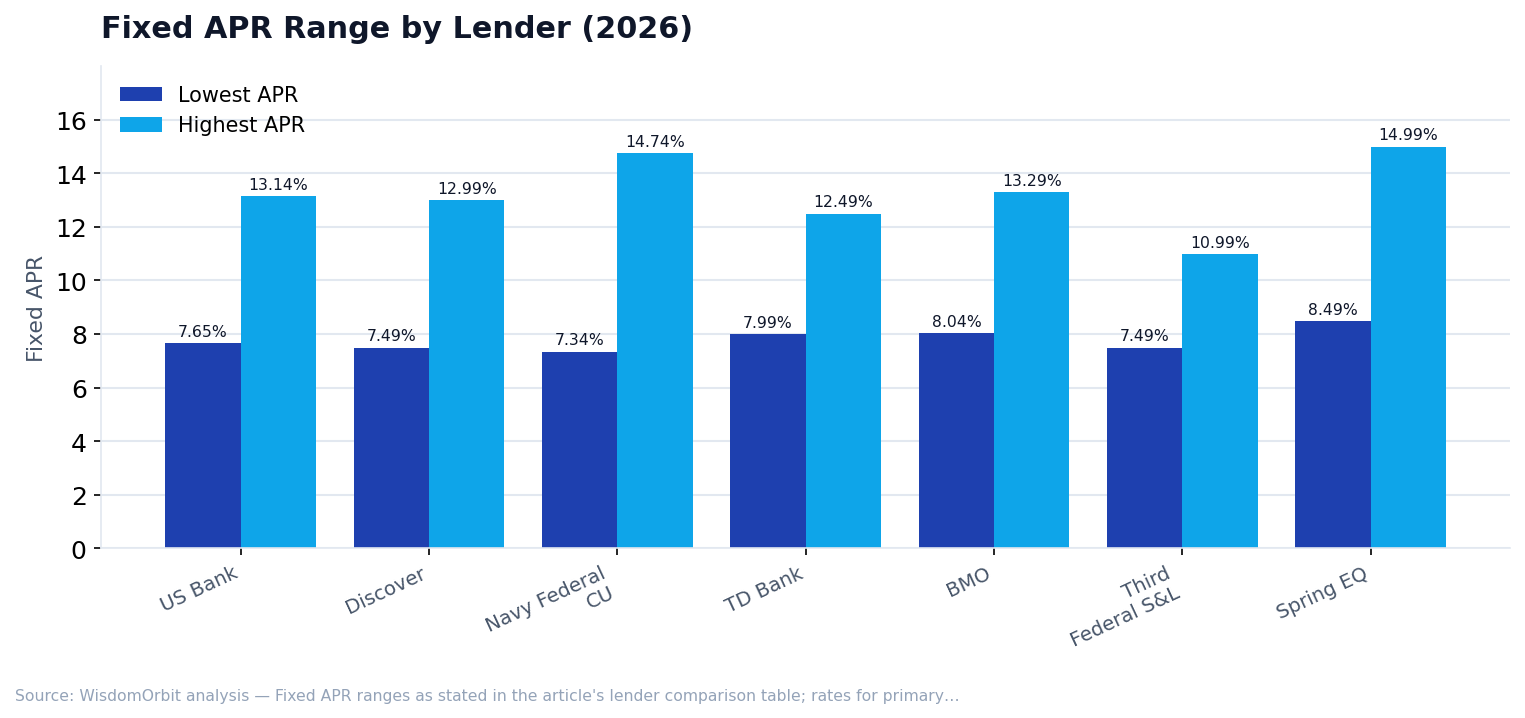

Best Home Equity Loan Lenders 2026: Side-by-Side Comparison

We evaluated seven of the most widely available home equity loan lenders on the criteria that matter most: rates, fees, maximum LTV, loan amounts, and borrower experience. Here is how they stack up.

Rates shown are for primary residences with excellent credit (740+). Your rate will depend on credit score, CLTV, loan amount, and term. Rates current as of March 2026; verify directly with lenders.

Home Equity Loan vs. HELOC: Which Should You Choose?

This is one of the most common questions borrowers ask. Both products tap your home's equity, but they work very differently. Here is a direct comparison:

Bottom line: Choose a home equity loan when you know the exact amount you need and want payment certainty. Choose a HELOC when you need flexibility — for example, financing a renovation project where costs may change over time.

How to Qualify for a Home Equity Loan

Lenders evaluate four main criteria when you apply for a home equity loan. Meeting or exceeding these benchmarks will improve your chances of approval and help you secure a lower rate.

1. Sufficient Home Equity

You generally need at least 15% to 20% equity remaining after the loan. Most lenders cap your CLTV at 80%–85%, though some (Navy Federal, Spring EQ) go higher. Your equity is verified through a professional appraisal or, increasingly, an automated valuation model (AVM).

2. Credit Score of 620 or Higher

The minimum credit score for most home equity loans is 620, though some lenders set the floor at 660 or 680. Here is how your score affects pricing:

3. Debt-to-Income Ratio Below 43%

Your debt-to-income ratio (DTI) measures your total monthly debt payments — including the proposed home equity loan payment — divided by your gross monthly income. Most lenders cap DTI at 43%, though some allow up to 50% with compensating factors like a high credit score or low CLTV.

Example: If your gross monthly income is $8,000 and your total monthly debts (mortgage, car payment, credit card minimums, new home equity loan payment) total $3,200, your DTI is 40% — within most lenders' guidelines.

4. Stable Income and Employment

Lenders typically want to see at least two years of consistent income. W-2 employees will provide pay stubs and tax returns. Self-employed borrowers generally need two years of tax returns and may face additional scrutiny of income stability.

Application Process: Step by Step

The home equity loan process typically takes 2 to 6 weeks from application to funding. Here is what to expect at each stage.

Step 1: Check Your Equity and Credit (Day 1)

Before applying, estimate your home's current value using tools like Zillow's Zestimate or Redfin's estimate (keeping in mind these are rough guides, not appraisals). Pull your free credit report at AnnualCreditReport.com and check your FICO score. This helps you gauge which lenders to target and what rate to expect.

Step 2: Compare Lenders and Get Pre-Quotes (Days 1–3)

Request rate quotes from at least three lenders. Multiple credit inquiries for mortgage products within a 14-day window count as a single inquiry on your credit report (per FICO scoring models), so there is no penalty for shopping around. Compare APR (not just interest rate), closing costs, and terms.

Step 3: Submit Your Application (Day 3–5)

You will need to provide:

- Government-issued ID

- Most recent mortgage statement

- Last two years of W-2s or tax returns

- Recent pay stubs (last 30 days)

- Bank statements (last 2–3 months)

- Homeowners insurance declaration page

Step 4: Home Appraisal (Week 1–3)

The lender will order an appraisal to verify your home's value. Traditional in-person appraisals cost $300 to $600 and take 1 to 3 weeks depending on your market. Some lenders (like Discover) waive the appraisal fee or use an AVM for qualifying properties, which can speed this step to just a few days.

Step 5: Underwriting and Closing (Week 2–6)

Once the appraisal is complete, the underwriter reviews your full file. If everything checks out, you will receive a closing disclosure at least three business days before closing (as required by the TILA-RESPA Integrated Disclosure rule). At closing, you sign the loan documents, and funds are typically disbursed within 3 business days.

Important: Under federal law, you have a 3-business-day right of rescission after closing. During this period, you can cancel the loan for any reason without penalty. This right applies to home equity loans on primary residences only.

Costs and Fees to Expect

Home equity loans come with closing costs that typically range from 2% to 5% of the loan amount. On a $50,000 loan, expect $1,000 to $2,500 in total closing costs. Here is a breakdown of common fees:

Pro tip: Some lenders (Discover, Third Federal) cover all or most closing costs to win your business. This can save you $1,000+ upfront, though it may be reflected in a slightly higher rate. Always compare the total cost of the loan, not just the rate or fees in isolation.

Tax Deduction Rules for Home Equity Loans

The tax treatment of home equity loan interest changed significantly with the Tax Cuts and Jobs Act (TCJA) of 2017. Here is what you need to know for your 2026 tax return:

- Deductible: Interest on home equity loan proceeds used to buy, build, or substantially improve the home securing the loan. This includes kitchen remodels, room additions, roof replacements, and similar capital improvements.

- Not deductible: Interest on proceeds used for other purposes, such as paying off credit cards, funding a vacation, covering college tuition, or buying a car.

- Debt limit: The total of your primary mortgage plus home equity loan cannot exceed $750,000 ($375,000 if married filing separately) for the interest to be deductible. For mortgages taken out before December 16, 2017, the limit is $1,000,000.

Per IRS Publication 936, you should keep detailed records of how you use the loan proceeds. Save receipts, contractor invoices, and photos of improvements. This documentation protects you in case of an audit.

Pros and Cons of Home Equity Loans

Pros

- Fixed rate means predictable monthly payments

- Lower rates than credit cards or personal loans (typically 5–8% cheaper)

- Interest may be tax-deductible for home improvements

- Large borrowing capacity ($10K–$750K at top lenders)

- Lump sum is ideal for known, one-time costs

- Long repayment terms (up to 30 years) keep monthly payments manageable

Cons

- Your home is collateral — risk of foreclosure if you default

- Closing costs of 2%–5% add upfront expense

- Reduces your equity cushion and increases total debt

- Rates are higher than primary mortgages (second lien risk)

- Appraisal may come in lower than expected, limiting borrowing

- Not flexible — you borrow once and cannot draw more later

When a Home Equity Loan Makes Sense (and When It Does Not)

Good Uses for a Home Equity Loan

- Major home renovations: Kitchen remodels ($25K–$80K), bathroom renovations ($15K–$40K), and additions can increase your home's value while being funded at favorable rates with potentially deductible interest.

- Debt consolidation: If you carry $30,000 in credit card debt at 22% APR, consolidating it into an 8.5% home equity loan could save you over $4,000 per year in interest — just make sure you do not run the cards back up.

- Emergency large expense: Major medical bills or essential home repairs (roof, foundation, HVAC) where the cost is known and the alternative is higher-rate debt.

When to Consider Alternatives

- Uncertain costs: If you do not know the exact amount needed, a HELOC offers more flexibility.

- Small amounts: For less than $10,000, a personal loan or 0% APR credit card may be simpler and cheaper after accounting for closing costs.

- Short-term need: If you can repay within 12–18 months, the closing costs of a home equity loan may exceed the interest savings. A personal loan with no origination fee could be more cost-effective.

- Low equity: If your CLTV would exceed 85%, you will face limited lender options and higher rates. It may be better to wait until you have built more equity.

- Unstable income: Putting your home at risk when your income is uncertain is rarely advisable.

Worked Example: $50,000 Home Equity Loan for a Kitchen Remodel

Lisa owns a home appraised at $425,000 with $260,000 remaining on her mortgage. She wants to borrow $50,000 for a kitchen renovation.

- CLTV: ($260,000 + $50,000) / $425,000 = 72.9% — well within the 80% threshold

- Credit score: 755 — qualifies for competitive rates

- Rate offered: 8.25% fixed for 15 years

- Monthly payment: approximately $485

- Total interest paid: approximately $37,300 over 15 years

- Closing costs: approximately $1,200 (lender waived appraisal fee)

- Tax benefit: Since proceeds are used for home improvement, interest is deductible. In the 24% tax bracket, this saves roughly $8,950 over the life of the loan.

- Net cost after tax savings: approximately $29,550 in interest

Compare this to funding the same renovation on a credit card at 22% APR: the credit card would cost over $100,000 in interest on a 15-year payoff. The home equity loan saves Lisa more than $70,000.

Editor’s Insight

Home equity loans remain one of the most cost-effective ways to borrow a large sum in 2026, but only if you use them strategically. The fixed rate is a genuine advantage in an uncertain rate environment — you lock in your cost and your payment never changes. However, too many homeowners treat their equity like an ATM, borrowing for consumption rather than investment. The best use of a home equity loan is one that either increases your home's value (renovations), eliminates far more expensive debt (consolidation), or addresses a true necessity. If you cannot clearly articulate how the loan improves your financial position, you should probably not take it.

Frequently Asked Questions

What is the difference between a home equity loan and a HELOC?

A home equity loan gives you a lump sum at a fixed interest rate with predictable monthly payments over a set term (typically 5 to 30 years). A HELOC (home equity line of credit) works like a credit card: you get a revolving credit line with a variable rate and draw funds as needed during a draw period (usually 10 years), followed by a repayment period. Home equity loans are better for one-time expenses with a known cost, while HELOCs suit ongoing or unpredictable expenses.

How much equity do I need to qualify for a home equity loan?

Most lenders require at least 15% to 20% equity in your home after the loan. This means your combined loan-to-value ratio (CLTV) — your mortgage balance plus the new home equity loan divided by your home's appraised value — generally cannot exceed 80% to 85%. Some lenders like Navy Federal allow up to 100% CLTV for qualifying borrowers, though this typically comes with higher rates.

Is home equity loan interest tax-deductible?

Yes, but only if you use the funds to "buy, build, or substantially improve" the home that secures the loan. Under the Tax Cuts and Jobs Act of 2017, interest on up to $750,000 of total qualified mortgage debt (including home equity loans) is deductible if the proceeds are used for home improvements. Interest on funds used for other purposes — such as paying off credit cards or covering tuition — is not deductible. Consult a tax professional for your specific situation.

What credit score do I need for the best home equity loan rates?

To qualify for the lowest advertised rates, most lenders require a credit score of 740 or higher. You can generally qualify for a home equity loan with a score of 620 to 680, but you will pay a higher interest rate — often 1 to 3 percentage points more than the best available rate. Improving your score before applying can save thousands of dollars over the life of the loan.

How long does it take to get a home equity loan?

The typical home equity loan closing timeline is 2 to 6 weeks from application to funding. The process includes application review, income and asset verification, a home appraisal (which alone can take 1 to 3 weeks depending on your market), title search, underwriting, and closing. Online lenders like Discover tend to close faster (sometimes in as few as 2 to 3 weeks), while traditional banks may take the full 4 to 6 weeks.

You May Also Like

Sources & References

- Federal Reserve — Federal Funds Rate target range

- IRS — Publication 936: Home Mortgage Interest Deduction

- Consumer Financial Protection Bureau (CFPB) — Home Loan Toolkit and TILA-RESPA Disclosure Rules

- FDIC — Consumer guidance on home equity products

- Bankrate — Home equity loan rate surveys and lender data, accessed March 2026

- Individual lender websites — US Bank, Discover, Navy Federal, TD Bank, BMO, Third Federal, Spring EQ rate pages accessed March 2026