Key Takeaways

- VA loans require zero down payment and no private mortgage insurance (PMI), potentially saving veterans tens of thousands of dollars over the life of a loan.

- Eligible veterans with full entitlement face no loan limit in 2026 — you can borrow as much as a lender will approve.

- VA loan interest rates average 0.25% to 0.5% lower than conventional mortgages, translating to significant long-term savings.

- The VA funding fee ranges from 0.5% to 3.3% depending on usage and down payment, but disabled veterans and Purple Heart recipients are exempt.

- VA loans can be used multiple times — entitlement is restorable, and you can even have more than one VA loan simultaneously with remaining entitlement.

What Is a VA Home Loan?

A VA home loan is a mortgage option backed by the U.S. Department of Veterans Affairs, designed specifically for veterans, active-duty service members, certain National Guard and Reserve members, and eligible surviving spouses. It is one of the most valuable financial benefits earned through military service.

Contrary to a common misconception, the VA does not directly lend money to borrowers. Instead, the VA guarantees a portion of the loan — typically up to 25% of the conforming loan limit — made by private lenders such as banks, credit unions, and mortgage companies. This guarantee protects lenders against loss if the borrower defaults, which is why VA loans come with such favorable terms.

The VA loan program traces its roots to the Servicemen's Readjustment Act of 1944, more commonly known as the GI Bill. President Franklin D. Roosevelt signed this landmark legislation to help returning World War II veterans reintegrate into civilian life. Since its inception, the program has facilitated over 28 million VA-guaranteed home loans, helping generations of military families achieve homeownership.

The program has evolved significantly over the decades. Recent legislative changes — most notably the Blue Water Navy Vietnam Veterans Act of 2019 — eliminated loan limits for eligible veterans with full entitlement, making the benefit even more powerful in today's high-cost housing market.

Key Benefits of VA Loans

VA home loans are widely considered the most advantageous mortgage product available in the United States. Here is a detailed breakdown of each major benefit:

Zero Down Payment

This is the single largest advantage of a VA loan. While conventional mortgages typically require a down payment of 3% to 20% of the purchase price, VA loans allow eligible borrowers to finance 100% of the home's value. On a $400,000 home, that means saving between $12,000 and $80,000 in upfront cash — money that can instead go toward moving costs, furnishing, or an emergency fund.

No Private Mortgage Insurance (PMI)

Conventional borrowers who put down less than 20% are required to pay PMI, which typically costs between $100 and $300 per month on a $300,000 loan. Over the years it takes to build 20% equity, that can add up to $15,000 or more in unnecessary costs. VA loans completely eliminate this requirement, regardless of your down payment amount.

Competitive Interest Rates

Because the VA guaranty reduces lender risk, VA loans consistently offer interest rates that are 0.25% to 0.5% lower than comparable conventional mortgages. On a $350,000 30-year fixed loan, a 0.5% rate reduction saves approximately $35,000 in interest over the life of the loan.

Limited Closing Costs

The VA places strict limits on what fees lenders can charge VA borrowers. The origination fee is capped at 1% of the loan amount, and certain fees — such as attorney fees, prepayment penalties, and broker commissions — are either restricted or prohibited entirely. Sellers are permitted to pay up to 4% of the loan amount toward the buyer's closing costs and concessions.

No Prepayment Penalty

VA borrowers can pay off their loan early — whether through additional monthly payments, lump-sum payments, or refinancing — without incurring any penalties. This gives veterans maximum flexibility to reduce their mortgage costs as their financial situation improves.

Assumable Loans

VA loans are assumable, meaning the loan can be transferred to another buyer — including non-veterans — subject to VA and lender approval. In a rising interest rate environment, an assumable VA loan at a lower rate can be a significant selling point and add value to your property.

VA Loan Types

Purchase Loans

The most common VA loan type, used to buy a primary residence. Eligible properties include single-family homes, condominiums (in VA-approved projects), manufactured homes on permanent foundations, and multi-unit properties up to four units — provided the borrower occupies one unit as their primary residence.

Interest Rate Reduction Refinance Loan (IRRRL)

Also known as a VA Streamline Refinance, the IRRRL is designed to lower your interest rate on an existing VA loan with minimal paperwork and typically no appraisal, no income verification, and no credit underwriting. The funding fee is just 0.5%, making it one of the most cost-effective refinancing options available. You must demonstrate a tangible net benefit — usually a rate reduction of at least 0.5%.

Cash-Out Refinance

This option allows veterans to refinance an existing mortgage (VA or non-VA) and take cash out from their home's equity. Borrowers can refinance up to 100% of the home's appraised value in many cases. This is commonly used for home improvements, debt consolidation, or covering major expenses like education.

Native American Direct Loan (NADL)

The NADL program is a direct loan from the VA — one of the few instances where the VA acts as the actual lender. It helps eligible Native American veterans purchase, build, or improve homes on Federal Trust Land. Interest rates are set by the VA and are generally competitive with or better than private market rates.

Adapted Housing Grants

While not technically a loan, the VA offers two grant programs for veterans with certain service-connected disabilities. The Specially Adapted Housing (SAH) grant helps build or modify a home for wheelchair accessibility; the grant maximum is adjusted every fiscal year (see va.gov/housing-assistance for the current cap). The Special Housing Adaptation (SHA) grant covers less extensive modifications, with a separate annually-adjusted maximum (current figures at va.gov).

Eligibility Requirements

Eligibility for a VA home loan depends on your service history, duty status, and character of discharge. Below is a detailed breakdown by service category:

| Service Category | Minimum Service Requirement | Additional Notes |

|---|---|---|

| Active Duty | 90 continuous days (wartime) or 181 continuous days (peacetime) | Currently serving members are eligible after minimum service period |

| Veterans | Same as active duty + honorable discharge | Other-than-dishonorable may qualify on case-by-case basis |

| National Guard / Reserves | 6 years of service or 90 days active duty under Title 10 | Title 10 activation during Gulf War era or later qualifies at 90 days |

| Surviving Spouses | N/A | Unremarried spouse of veteran who died in service or from service-connected disability; spouse who remarried after age 57 may also qualify |

Certificate of Eligibility (COE)

Before applying for a VA loan, you need to obtain a Certificate of Eligibility (COE) to verify your entitlement. There are three ways to get your COE:

- Online at VA.gov — The fastest method; instant results for most veterans and active-duty members whose records are in the VA system.

- Through your lender — Most VA-approved lenders can obtain your COE electronically using the VA's Web LGY system, often within minutes.

- By mail — Submit VA Form 26-1880 with proof of service (DD-214 for veterans) to the VA's Eligibility Center in Winston-Salem, NC. This method takes approximately 4 to 6 weeks.

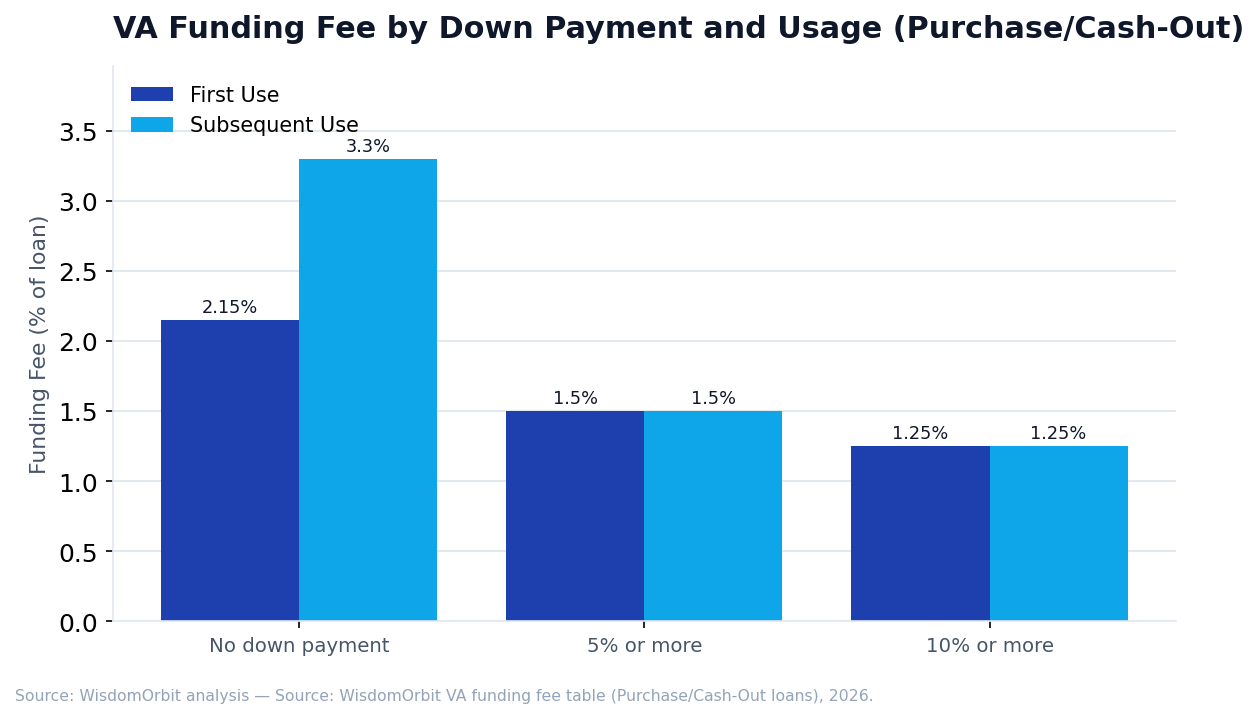

VA Funding Fee

The VA funding fee is a one-time payment that helps sustain the VA loan program for future generations of veterans. The fee varies based on several factors: whether it is your first time using the benefit, your down payment amount, and your branch of service. The fee can be paid upfront at closing or rolled into the loan balance.

| Loan Type | Down Payment | First Use (Regular) | First Use (Reserves/Guard) | Subsequent Use |

|---|---|---|---|---|

| Purchase / Cash-Out | None | 2.15% | 2.15% | 3.3% |

| Purchase / Cash-Out | 5% or more | 1.5% | 1.5% | 1.5% |

| Purchase / Cash-Out | 10% or more | 1.25% | 1.25% | 1.25% |

| IRRRL (Streamline) | N/A | 0.5% | 0.5% | 0.5% |

Funding Fee Exemptions

The following groups are exempt from paying the VA funding fee:

- Veterans receiving VA disability compensation for a service-connected disability rated at 10% or higher

- Veterans who would be entitled to disability compensation but receive retirement or active-duty pay instead

- Purple Heart recipients serving on active duty

- Surviving spouses receiving Dependency and Indemnity Compensation (DIC)

2026 VA Loan Limits

Since the passage of the Blue Water Navy Vietnam Veterans Act on January 1, 2020, eligible veterans with full entitlement have no loan limit. This means if you have never used your VA loan benefit — or have restored your full entitlement after paying off a previous VA loan — you can borrow as much as a VA-approved lender will extend to you, with no down payment required.

However, loan limits still apply to veterans with reduced or partial entitlement — those who have an active VA loan or have not fully restored their entitlement. For these borrowers, the 2026 limit is tied to the Federal Housing Finance Agency's conforming loan limit: FHFA baseline conforming limit (adjusted annually — see fhfa.gov), with higher limits in designated high-cost areas (up to $1,149,825 in the most expensive markets like San Francisco, New York City, and parts of Hawaii).

How Partial Entitlement Works

Every eligible veteran has a basic entitlement of $36,000 and a bonus (or "tier 2") entitlement that brings the total guarantee up to 25% of the conforming loan limit. If part of your entitlement is currently tied up in an existing VA loan, the remaining entitlement determines how much you can borrow on a second VA loan without a down payment.

For example, if you have $100,000 of entitlement remaining and the conforming loan limit in your county is, for example, $766,550, you could borrow up to approximately $400,000 on a second VA loan with zero down. Any amount above that would require a down payment of 25% of the difference.

Top VA Loan Lenders Comparison (2026)

Not all VA lenders are created equal. Rates, fees, service quality, and borrower requirements vary significantly. Here is a comparison of the leading VA loan lenders in 2026:

| Lender | Min Credit Score | Avg Rate Range | Unique Feature | Best For |

|---|---|---|---|---|

| Veterans United | 620 | 5.75%–6.50% | Largest VA lender, A+ BBB rating, free credit counseling | First-time VA borrowers |

| Navy Federal CU | 620 | 5.50%–6.25% | Low rates, no origination fee on certain loans | Military-affiliated members seeking lowest rates |

| USAA | 620 | 5.625%–6.375% | Full-service military bank, exceptional customer service | Existing USAA members |

| Rocket Mortgage | 580 | 5.875%–6.625% | Fully digital process, fast pre-approval | Tech-savvy borrowers, lower credit scores |

| PenFed Credit Union | 620 | 5.625%–6.50% | Open to all (not just military), competitive jumbo VA rates | Jumbo VA loans, non-military co-borrowers |

| loanDepot | 580 | 5.75%–6.75% | Flexible underwriting, lifetime refinance guarantee | Borrowers needing flexible qualification |

Note: Rate ranges are indicative only and vary based on credit profile, loan amount, and market conditions. Always request a Loan Estimate from multiple lenders to compare actual rates and fees.

The VA Loan Process Step by Step

Understanding the VA loan process from start to finish helps set realistic expectations and avoid common pitfalls. The typical timeline is 30 to 45 days from pre-approval to closing, though this varies by lender and market conditions.

Step 1: Obtain Your Certificate of Eligibility (COE)

Your COE verifies your VA loan entitlement. As mentioned earlier, the fastest method is through your lender's electronic access to the VA's Web LGY system, which often returns results in minutes. Having your COE ready before shopping for homes strengthens your position as a buyer.

Step 2: Get Pre-Approved

Pre-approval involves a lender reviewing your credit, income, debts, and employment to determine how much you can borrow. This is more thorough than pre-qualification and carries more weight with sellers. A pre-approval letter shows sellers you are a serious, financially vetted buyer.

Step 3: Find Your Home

Work with a real estate agent, preferably one experienced with VA transactions. The property must serve as your primary residence — VA loans cannot be used for vacation homes or pure investment properties. Remember that multi-unit properties (up to four units) are eligible if you live in one unit.

Step 4: VA Appraisal

After your offer is accepted, the lender orders a VA appraisal through the VA's appraisal management system. This is a critical step unique to VA loans. The VA-assigned appraiser evaluates two things: the property's market value and whether it meets the VA's Minimum Property Requirements (MPRs). The property must be safe, sanitary, and structurally sound. Common MPR issues include peeling paint (for homes built before 1978), inadequate heating systems, roof damage, and pest infestations.

Step 5: Underwriting

The lender's underwriting team performs a final review of all documentation — income verification, asset statements, credit history, and the appraisal report. VA loans use a residual income calculation in addition to the standard debt-to-income (DTI) ratio. Residual income measures how much disposable income you have after all major expenses, and is one reason VA loans have historically low default rates.

Step 6: Closing

At closing, you sign the final loan documents, pay any closing costs not covered by seller concessions or lender credits, and receive the keys to your new home. The VA funding fee (if applicable) is typically financed into the loan at this stage.

VA Appraisal vs. Home Inspection

This is one of the most misunderstood aspects of the VA loan process. Many buyers confuse the VA appraisal with a home inspection — they serve very different purposes.

The VA appraisal is required by the lender and the VA. Its primary purposes are to establish the property's fair market value (to protect the VA's investment) and to verify that the home meets MPRs. However, the VA appraiser is not conducting a comprehensive inspection — they are looking at the property at a surface level for obvious safety and structural issues.

A home inspection, by contrast, is optional but strongly recommended. A licensed home inspector will spend 2 to 4 hours examining the property's systems in detail — electrical, plumbing, HVAC, foundation, roof, appliances, and more. The inspector can identify issues that a VA appraiser would never catch, such as hidden water damage, aging electrical wiring, or a furnace nearing the end of its lifespan.

The Tidewater Procedure

If a VA appraiser determines that the property's value may come in lower than the purchase price, they are required to invoke the Tidewater Procedure before issuing a final value. This gives the buyer's agent and lender 48 hours to submit additional comparable sales data that might support a higher valuation. If the appraisal still comes in low, the buyer has several options: negotiate a lower price with the seller, pay the difference out of pocket, request a Reconsideration of Value (ROV) with new comps, or walk away from the deal using an appraisal contingency.

Common VA Loan Myths Debunked

Myth: "VA Loans Take Too Long to Close"

This was more true a decade ago, but modern VA lending has largely closed the gap. According to data from ICE Mortgage Technology, VA loans average approximately 48 days to close compared to 47 days for conventional loans — a negligible difference. Well-organized borrowers with responsive lenders routinely close VA loans in 30 days or less.

Myth: "Sellers Don't Want VA Offers"

Some seller reluctance exists, particularly in hot markets, due to concerns about VA appraisals and repair requirements. However, this has improved significantly. The National Association of Realtors reports that VA buyers represent approximately 6% to 7% of all home purchases, and many sellers — especially those whose homes are in good condition — readily accept VA offers. A strong pre-approval letter and competitive offer price can overcome any remaining hesitation.

Myth: "You Can Only Use a VA Loan Once"

Completely false. VA loan entitlement is a reusable benefit. Once you sell a VA-financed home and pay off the loan, your full entitlement is typically restored through a one-time restoration process. You can even have two VA loans simultaneously if you have sufficient remaining entitlement — a common scenario for service members who receive PCS (Permanent Change of Station) orders.

Myth: "VA Loans Are Only for First-Time Homebuyers"

There is no first-time buyer requirement for VA loans. Whether you are purchasing your first home, your fifth, or refinancing an existing mortgage, the VA loan benefit is available as long as you meet eligibility requirements and have entitlement available.

Frequently Asked Questions

Can I use a VA loan more than once?

Yes. VA loan entitlement can be restored and reused multiple times throughout your lifetime. Once you sell a previous VA-financed home and pay off the loan, your full entitlement is typically restored through a simple one-time restoration process. You can even have more than one VA loan at a time if you have remaining entitlement — a common situation for military members who PCS to a new duty station and want to keep their previous home as a rental.

Is there a VA loan limit in 2026?

For veterans with full entitlement, there is no loan limit — you can borrow as much as a lender will approve with no down payment required. For those with reduced entitlement (for example, if you have a previous VA loan that has not been paid off), the limit is tied to the FHFA conforming loan limit for your county, which is adjusted every year (check fhfa.gov for the current figure), with higher limits in designated high-cost counties reaching up to $1,149,825.

Do I have to pay the VA funding fee?

Most borrowers pay the VA funding fee, which ranges from 0.5% for an IRRRL to 3.3% for subsequent-use purchase loans with no down payment. However, several groups are exempt: veterans receiving VA disability compensation at a 10% or higher rating, Purple Heart recipients on active duty, and surviving spouses receiving DIC benefits. If you believe you may qualify for an exemption, discuss this with your lender before closing.

Can I use a VA loan for an investment property?

VA loans require owner-occupancy — you must certify your intent to live in the property as your primary residence within 60 days of closing. Pure investment properties are not eligible. However, you can purchase a multi-unit property (up to four units) using a VA loan, live in one unit, and rent out the remaining units. This is a popular strategy for building rental income while using the VA loan benefit.

What credit score do I need for a VA loan?

The VA itself does not set a minimum credit score requirement, which is unique among major loan programs. However, individual lenders set their own minimums, which typically range from 580 to 660. Lenders like Rocket Mortgage and loanDepot may accept scores as low as 580, while Veterans United, Navy Federal, and USAA generally look for 620 or higher. If your credit score is below 620, focus on improving it before applying — even a small increase can qualify you for better rates and more lender options.

Editor's Insight

The most common mistake veterans make is not shopping multiple VA-approved lenders. The difference between the best and worst VA loan offers can be staggering — industry pricing data shows rate spreads of over 0.75% and origination fee differences of several thousand dollars on the same borrower profile. Always get Loan Estimates from at least three lenders before committing.

The second most costly mistake is skipping the home inspection because "the VA appraisal covers it." It does not. Buyers regularly close on homes that passed the VA appraisal only to discover $15,000 in plumbing issues or a failing HVAC system within the first year. The $400 to $600 cost of a professional home inspection is the best money you will spend during the entire process.

Finally, if you have any service-connected disability rating, apply for your VA funding fee exemption before closing — not after. Getting a refund retroactively is possible but involves paperwork and delays that are easily avoided with proper planning.

Sources

- U.S. Department of Veterans Affairs. "VA Home Loans." va.gov/housing-assistance/home-loans

- Consumer Financial Protection Bureau. "Explore Interest Rates — VA Loans." consumerfinance.gov

- Veterans United Home Loans. "VA Loan Statistics and Research." veteransunited.com/education

- National Association of Realtors. "Profile of Home Buyers and Sellers — VA Buyer Data." nar.realtor/research-and-statistics

- Federal Housing Finance Agency. "2026 Conforming Loan Limits." fhfa.gov/data/conforming-loan-limits

- ICE Mortgage Technology. "Origination Insight Report — Average Days to Close." icemortgagetechnology.com