Business insurance protects companies from financial losses due to lawsuits, property damage, employee injuries, and other risks that could otherwise devastate or bankrupt an organization. Whether you're a sole proprietor, small business owner, or managing a large corporation, the right insurance coverage is essential for long-term stability and peace of mind.

This comprehensive guide covers the main types of business insurance, what each policy covers, how much coverage costs, and how to determine which policies your business needs.

Why Business Insurance Matters

A single lawsuit, accident, or disaster can cost hundreds of thousands of dollars or more. Without proper insurance:

- Legal defense - Defending against even frivolous lawsuits costs $50,000-$100,000+ in legal fees

- Property losses - Fire, theft, or natural disasters could destroy inventory and equipment

- Liability claims - Customer injuries or property damage claims can result in massive judgments

- Business interruption - Extended closures from disasters mean no revenue while expenses continue

- Employee claims - Workers' compensation claims, discrimination suits, and wrongful termination cases

Beyond protection, many situations require business insurance: landlords typically require it for commercial leases, clients may require proof of coverage before signing contracts, and some industries have mandatory insurance requirements.

Types of Business Insurance

General Liability Insurance

The foundation of business insurance, general liability protects against third-party claims for bodily injury, property damage, and personal injury (like defamation). If a customer slips in your store, a delivery driver damages a client's property, or someone claims your advertising injured their reputation, general liability responds.

What it covers:

- Customer injuries on your premises

- Damage to others' property caused by your business operations

- Advertising injury (libel, slander, copyright infringement)

- Legal defense costs

- Medical payments for minor injuries

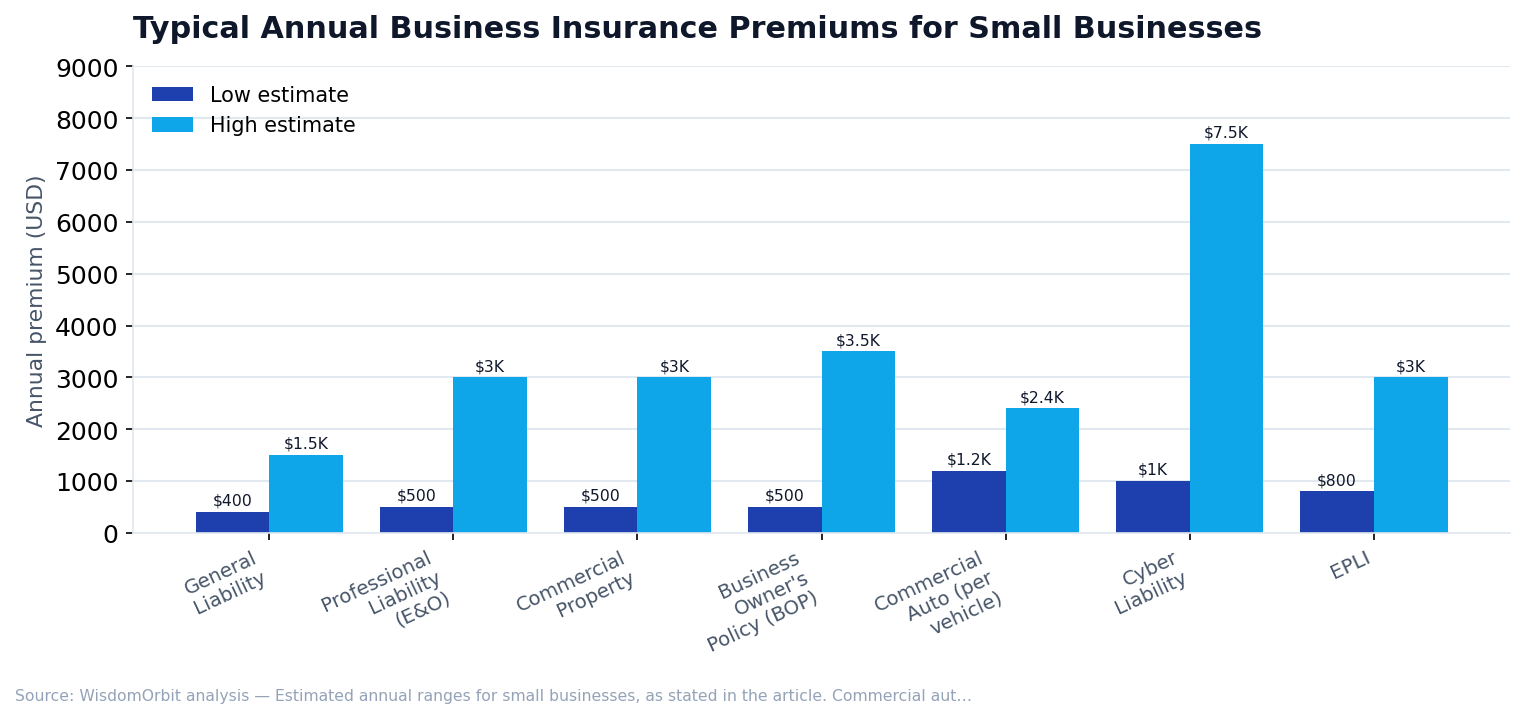

Typical cost: $400-$1,500 per year for small businesses, depending on industry and coverage limits.

Professional Liability Insurance (Errors & Omissions)

Essential for service-based businesses, professional liability covers claims arising from mistakes, negligence, or failure to deliver services as promised. Unlike general liability, which covers physical harm, E&O covers financial harm from professional services.

Who needs it:

- Consultants and advisors

- IT professionals and developers

- Accountants and financial advisors

- Architects and engineers

- Real estate agents

- Healthcare providers (malpractice insurance)

Typical cost: $500-$3,000+ per year depending on profession and coverage.

Commercial Property Insurance

Protects your business's physical assets including buildings, equipment, inventory, furniture, and fixtures against fire, theft, vandalism, and certain natural disasters. If you own your building or have significant equipment/inventory, property insurance is essential.

Coverage options:

- Named perils - Only covers specific listed events (fire, theft, etc.)

- Open perils (all-risk) - Covers everything except specifically excluded events

- Replacement cost - Pays to replace items at current prices

- Actual cash value - Pays depreciated value of items

Typical cost: $500-$3,000+ per year based on property value and location.

Business Owner's Policy (BOP)

A bundled policy combining general liability and commercial property insurance at a discounted rate. BOPs are designed for small to medium businesses and offer convenient, cost-effective coverage. Many BOPs also include business interruption coverage.

Best for: Small businesses with physical locations, retail stores, restaurants, and professional offices.

Typical cost: $500-$3,500 per year - usually 10-15% less than buying policies separately.

Workers' Compensation Insurance

Required in almost every state if you have employees. Workers' comp covers medical expenses and lost wages when employees are injured on the job. It also protects employers from lawsuits by injured workers.

What it covers:

- Medical treatment for work-related injuries and illnesses

- Partial wage replacement during recovery

- Disability benefits for permanent impairment

- Death benefits for families of workers killed on the job

- Rehabilitation and retraining costs

Typical cost: $0.75-$2.50 per $100 of payroll, varying significantly by state and industry risk classification.

Commercial Auto Insurance

Required if your business owns vehicles or employees drive for work purposes. Personal auto policies typically exclude business use, making commercial coverage necessary.

Coverage types:

- Liability - Covers damage your vehicles cause to others

- Collision - Repairs to your vehicles after accidents

- Comprehensive - Non-collision damage (theft, weather, vandalism)

- Hired and non-owned auto - Covers employees using personal vehicles for work

Typical cost: $1,200-$2,400 per vehicle per year.

Cyber Liability Insurance

Increasingly essential as cyber attacks and data breaches affect businesses of all sizes. Cyber insurance covers costs associated with data breaches, ransomware attacks, and other cyber incidents.

What it covers:

- Data breach notification and credit monitoring for affected customers

- Forensic investigation costs

- Legal defense and regulatory fines

- Ransom payments (in some policies)

- Business interruption from cyber events

- Public relations and reputation management

Typical cost: $1,000-$7,500 per year for small businesses; higher for companies with sensitive data.

Business Interruption Insurance

Covers lost income when your business cannot operate due to a covered event (fire, natural disaster, etc.). While property insurance replaces your physical assets, business interruption replaces the revenue you lose while rebuilding.

What it covers:

- Lost net income during closure

- Operating expenses that continue (rent, utilities, loan payments)

- Extra expenses to minimize the closure period

- Employee wages to retain workers

Usually included in BOPs or added as an endorsement to property insurance.

Employment Practices Liability Insurance (EPLI)

Protects against employee claims of wrongful termination, discrimination, harassment, and other employment-related issues. With employment lawsuits increasingly common, EPLI has become essential for businesses with employees.

What it covers:

- Discrimination claims (age, race, gender, disability)

- Sexual harassment allegations

- Wrongful termination and retaliation

- Wage and hour disputes

- Failure to promote

Typical cost: $800-$3,000+ per year based on number of employees and claims history.

How Much Business Insurance Costs

Premium costs vary based on several factors:

- Industry - High-risk industries (construction, healthcare) pay more

- Business size - More employees and revenue means higher premiums

- Coverage limits - Higher limits cost more but provide better protection

- Claims history - Past claims typically increase future premiums

- Location - Areas prone to natural disasters or with high litigation rates cost more

- Deductible - Higher deductibles lower premiums but increase out-of-pocket costs

Determining What Coverage You Need

Minimum Coverage for Most Businesses

- General liability insurance

- Workers' compensation (if you have employees)

- Commercial auto (if vehicles are used for business)

Recommended Additional Coverage

- Commercial property insurance (if you have significant assets)

- Professional liability (if you provide advice or services)

- Cyber liability (if you store customer data)

- EPLI (if you have employees)

Industry-Specific Insurance

- Contractors - Builder's risk, contractor's liability, surety bonds

- Healthcare - Malpractice insurance

- Manufacturers - Product liability insurance

- Restaurants - Liquor liability, food contamination coverage

Tips for Getting the Best Business Insurance

- Compare multiple quotes - Get quotes from at least 3-5 insurers

- Work with a commercial insurance broker - They can access multiple markets and find specialized coverage

- Bundle policies - BOPs and package policies typically offer discounts

- Review annually - As your business grows, coverage needs change

- Understand exclusions - Know what's NOT covered before you need to file a claim

- Document everything - Maintain inventory records and photos to support claims

Frequently Asked Questions

Is business insurance tax deductible?

Yes, business insurance premiums are generally tax-deductible as ordinary business expenses. Consult with a tax professional for your specific situation.

Do I need business insurance if I work from home?

Yes. Homeowner's insurance typically excludes business activities. You'll need either a home-based business policy endorsement or separate business insurance.

How quickly can I get coverage?

Many policies can be bound the same day you apply, especially for small businesses with straightforward operations. More complex businesses may require underwriting that takes several days.

What happens if I'm sued and don't have insurance?

You'll be personally responsible for legal defense costs and any judgment against your business. This could mean losing personal assets if your business is a sole proprietorship or if corporate protections are pierced.

Sources & References

- Insurance Information Institute – Business Insurance Overview

- U.S. Small Business Administration – Business Insurance Guide

- National Association of Insurance Commissioners – Industry data and regulations