Key Takeaways

- SBA loans offer the lowest rates but require strong credit and patience

- Online lenders provide faster funding but at higher interest rates

- Prepare your business plan and financial statements before applying

Access to capital is crucial for business growth. Whether you're starting a new venture, expanding operations, purchasing equipment, or managing cash flow during slow periods, understanding your small business loan options can help you make the best financing decision for your situation. The right funding at the right time can accelerate growth; the wrong loan can burden your business with debt it can't handle.

Small businesses have more funding options than ever before. Traditional banks remain important, but online lenders, SBA-backed programs, and alternative financing have expanded access dramatically. This guide covers the major loan types, where to get them, qualification requirements, and how to choose the right financing for your needs.

Small Business Financing Options Compared (June 2026)

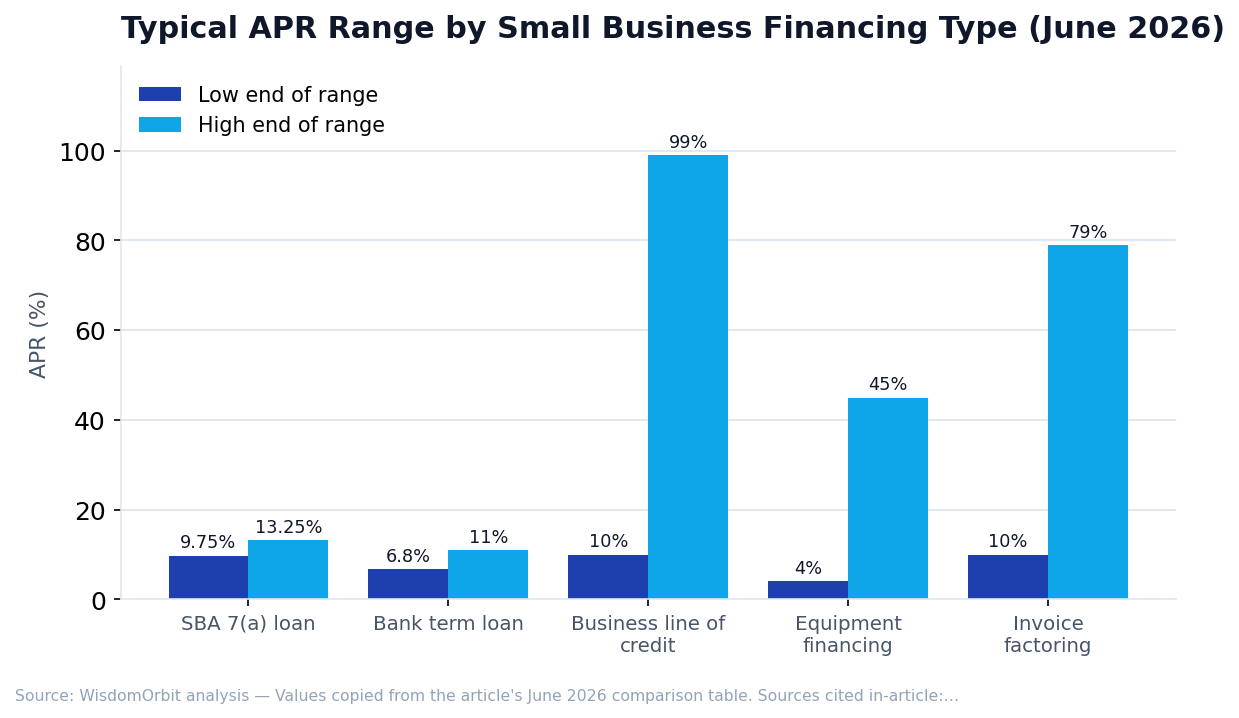

Here is how five common small-business financing options compare on cost, term length, and funding speed as of June 12, 2026, with SBA 7(a) rates anchored to the current 6.75% prime rate.

Sources: Federal Reserve H.15 release (bank prime loan rate 6.75%, data through June 10, 2026, federalreserve.gov/releases/h15); SBA 7(a) terms, conditions and eligibility (maximum spreads and maturities, sba.gov); NerdWallet — average business loan rates (updated June 1, 2026), typical small-business loan terms (updated Feb. 26, 2026), equipment financing (updated Apr. 30, 2026), invoice factoring (factor fees of 1%–5% of invoice value per month, updated Oct. 17, 2025), and best factoring companies of 2026 (cash within 24 hours once a factoring account is set up); Bankrate — bank business loan timelines ("SBA loans can take up to 90 days from the time of application to funding"; "most lenders take a few weeks," published Mar. 29, 2026) and online lenders funding as soon as the next business day. Rates vary by lender, credit profile, and loan size.

Types of Small Business Loans

SBA Loans

SBA loans are partially guaranteed by the Small Business Administration, which reduces risk for lenders and allows them to offer better terms to borrowers. The SBA doesn't lend directly; instead, banks and other lenders make loans under SBA programs.

The SBA 7(a) loan is the most popular program, offering up to $5 million for working capital, equipment, inventory, real estate, and refinancing. Terms extend up to 25 years for real estate and 10 years for equipment and working capital. Variable interest rates are capped at the prime rate plus a spread of 3.0-6.5 percentage points depending on loan size — roughly 9.75%-13.25% at the current 6.75% prime rate (see the June 2026 comparison table above) — keeping them among the lowest-cost options available.

SBA 504 loans specifically finance major fixed assets like real estate and equipment, with up to 90% financing and 10-25 year terms. SBA Microloans provide up to $50,000 for smaller funding needs, often available to businesses that don't qualify for larger loans.

The tradeoff: SBA loans require extensive documentation and can take 30-90 days for approval. They're best for established businesses with time to wait for competitive terms.

Term Loans

Traditional term loans provide a lump sum of capital that you repay over a fixed period with regular (usually monthly) payments of principal and interest. Terms typically range from 1-10 years, with shorter terms for smaller amounts and longer terms for larger loans or asset purchases.

Term loans are ideal for specific, planned investments: equipment purchases, expansion projects, inventory for a seasonal business, or acquiring another business. Fixed interest rates provide predictable payments, though variable-rate options exist. You receive all funds upfront and pay interest on the full amount from day one.

Business Lines of Credit

A line of credit gives you access to funds up to a certain limit that you can draw from as needed - similar to a credit card but typically with lower interest rates. You only pay interest on what you borrow, and as you repay, that credit becomes available again.

Lines of credit are perfect for managing cash flow fluctuations, covering unexpected expenses, or taking advantage of opportunities that require quick action. They're more flexible than term loans since you don't pay interest on funds you haven't used. Limits range from $10,000 to $500,000+, with terms from 6 months to several years.

Equipment Financing

Equipment loans use the equipment you're purchasing as collateral, which often results in easier approval and lower rates than unsecured financing. The equipment secures the loan, so if you default, the lender can repossess it.

Equipment financing typically covers 80-100% of the equipment cost with terms matching the equipment's useful life (3-7 years for most equipment, longer for vehicles or heavy machinery). Interest rates are competitive because the loan is secured. Down payments of 10-20% may be required for newer businesses or expensive equipment.

Invoice Factoring

If you have outstanding invoices from creditworthy customers, factoring allows you to sell those invoices to a factoring company at a discount for immediate cash. The factoring company then collects from your customers directly. This isn't a loan - you're selling an asset (the invoice).

Factoring is useful for B2B businesses with long payment cycles (30-90 days) who need faster access to working capital. Typical advance rates are 80-90% of invoice value, with fees of 1-5% depending on customer creditworthiness and payment terms. Quick access to cash is the advantage; the cost is higher than traditional loans.

Merchant Cash Advances

A merchant cash advance (MCA) provides a lump sum in exchange for a percentage of future credit card sales. Daily or weekly payments adjust based on your sales volume - you pay more when business is good, less when it's slow.

MCAs are fast (often funded within 24-48 hours) and accessible to businesses with lower credit scores, but they're expensive. Factor rates of 1.2-1.5 mean you repay $1,200-1,500 for every $1,000 borrowed. MCAs should be a last resort due to high costs.

Where to Get Small Business Loans

Traditional Banks

Banks like Wells Fargo, Chase, and Bank of America offer the lowest interest rates for qualified borrowers. They prefer established businesses with strong credit (680+ personal, good business credit), at least 2 years in business, solid revenue, and often collateral. The application process involves extensive documentation and can take weeks to months for approval.

Banks are best for established businesses with strong financials seeking the best rates and willing to invest time in the application process. Existing banking relationships often help approval odds.

Online Lenders

Online lenders like OnDeck, Fundbox, and Bluevine offer faster approval (often within 24-48 hours) with less stringent requirements than traditional banks. They use technology to streamline applications and underwriting, often connecting directly to your accounting software and bank accounts.

Interest rates are higher than banks (factor rates often used instead of APR, making true costs harder to compare), but accessibility makes online lenders popular for newer businesses, those with imperfect credit, or situations requiring quick funding. Terms tend to be shorter (3 months to 3 years).

Credit Unions

Credit unions often offer competitive rates with more personalized service than big banks. As member-owned nonprofits, they may be more flexible with businesses that have shorter track records or are located in underserved communities. Membership requirements apply (often based on location, employer, or association membership).

SBA-Approved Lenders

Banks, credit unions, and some online lenders participate in SBA loan programs. Preferred SBA lenders have authority to make approval decisions without SBA review, speeding the process. The SBA Lender Match tool connects you with participating lenders.

Alternative Lenders

Peer-to-peer lending platforms (like Funding Circle), revenue-based financing, and microloans from CDFIs (Community Development Financial Institutions) provide options for businesses that don't qualify elsewhere. Rates and terms vary widely, so compare carefully and understand total costs.

What You Need to Qualify

Most lenders evaluate these factors, though weighting varies:

- Credit Score - Personal credit is important for all small business loans. Most bank loans require 680+; some online lenders accept 550+. Business credit matters for larger, established companies.

- Time in Business - Banks typically want 2+ years; online lenders may accept 6 months to 1 year. Startups have limited options.

- Annual Revenue - Minimums range from $50,000 (online lenders) to $250,000+ (banks). Revenue demonstrates ability to repay.

- Debt Service Coverage Ratio - Your cash flow relative to existing debt payments. Lenders want to see that you can handle additional payments.

- Collateral - Assets to secure the loan. Required for some loans, helpful for better terms on others.

- Industry - Some industries (restaurants, retail, construction) are considered riskier. Restricted industries (cannabis, adult entertainment) have very limited options.

- Business Plan/Loan Purpose - Lenders want to understand how you'll use funds and how the investment will improve your ability to repay.

Current Interest Rates

Small business loan rates vary significantly by loan type, lender, and borrower qualifications:

- SBA 7(a) Loans - Prime + 3.0-6.5% depending on loan size (currently 9.75%-13.25% variable at the 6.75% prime rate)

- Bank Term Loans - 8-13% for well-qualified borrowers

- Online Term Loans - 15-80%+ (often expressed as factor rates)

- Business Lines of Credit - 10-80% depending on lender and qualifications

- Equipment Financing - 8-30% depending on credit and equipment type

- Invoice Factoring - 1-5% fee per invoice (not APR)

- Merchant Cash Advances - Factor rates of 1.2-1.5 (equivalent to 40-350% APR)

Documents Typically Required

- Business and personal tax returns (2-3 years)

- Business financial statements (P&L, balance sheet)

- Business bank statements (3-12 months)

- Business plan or loan purpose statement

- Proof of business ownership and legal documents

- Personal financial statement

- Collateral documentation (if applicable)

How to Apply

- Check your credit - Know your personal and business credit scores before applying

- Determine how much you need - Borrow what you need, not the maximum available

- Gather documents - Prepare financial statements, tax returns, and bank statements

- Compare multiple lenders - Get quotes from at least 3-5 lenders to compare rates and terms

- Understand total costs - Look beyond interest rates to fees, prepayment penalties, and total repayment amount

- Read terms carefully - Understand payment schedules, collateral requirements, and default consequences before signing

Frequently Asked Questions

Can I get a business loan with bad credit?

Yes, though options are limited and costs are higher. Online lenders and merchant cash advances accept lower credit scores. Secured loans (equipment financing, real estate) may be possible with collateral. Building credit before borrowing saves money long-term.

How much can I borrow?

Typical maximums based on loan type: SBA 7(a) up to $5 million; bank term loans $25,000-$500,000+; online lenders $5,000-$500,000; lines of credit $10,000-$500,000. Actual approval depends on your qualifications and ability to repay.

Should I use personal credit cards for business?

Generally no. Mixing personal and business finances can compromise your liability protection and makes accounting difficult. Business credit cards or lines of credit are better options for short-term business financing.

Getting Started

Start by understanding exactly how much you need and why. Then check your credit scores and gather basic financial documents. Research lenders appropriate for your situation - banks if you have strong qualifications and time, online lenders for speed or if qualifications are weaker. Always compare multiple offers, understanding the true total cost of each option, before committing to any loan.

Editor's Insight

Commercial lending analysts consistently point to the same mistake: business owners applying for too much money too soon. Lenders look at your debt service coverage ratio—your ability to make payments from existing cash flow. When you request more than your financials support, you either get declined or pushed toward expensive products like merchant cash advances.

My advice: Start with a smaller loan or line of credit to build your business credit profile. Pay it back on time, then apply for larger amounts. Banks reward track records. A business with two successful loans repaid is far more attractive than one applying for the first time asking for $500K.

Sources & References

- U.S. Small Business Administration – SBA Loan Programs Overview

- Federal Reserve Banks – Small Business Credit Survey (2024) – Reports that 43% of small businesses applied for financing, with approval rates varying significantly by lender type

- U.S. Bureau of Labor Statistics – Small business survival rates and financing trends

- Consumer Financial Protection Bureau – Small Business Lending Regulations

- National Federation of Independent Business (NFIB) – Monthly small business economic trends and credit availability reports

Related Articles

This article is for general information only and is not financial, legal, or tax advice. Verify current rates, fees, and terms with providers before making decisions.