A business line of credit gives you access to funds you can draw from as needed, paying interest only on what you use. Unlike term loans that provide a lump sum, lines of credit offer flexibility to borrow and repay repeatedly, making them one of the most versatile financing options for managing cash flow and unexpected expenses.

Think of a business line of credit like a credit card for your company, but typically with lower interest rates and higher limits. You have a set credit limit, draw funds when needed, pay them back, and your available credit replenishes. This revolving structure makes lines of credit ideal for businesses with fluctuating cash needs.

How Business Lines of Credit Work

Understanding the mechanics helps you use this financing tool effectively:

- Credit Limit - The maximum amount you're approved to borrow, typically ranging from $10,000 to $500,000 depending on your business qualifications

- Draw Period - The timeframe during which you can access funds, usually 12-24 months for online lenders, longer for banks

- Interest Charges - You only pay interest on the amount you've borrowed, not your total credit limit. Interest is typically calculated daily on your outstanding balance.

- Repayment - Make minimum payments (often weekly or monthly) to pay down your balance. Some lenders offer interest-only payments during the draw period.

- Revolving Credit - As you repay, those funds become available to borrow again. This cycle can continue as long as your line remains open.

Example: How It Works in Practice

You're approved for a $100,000 line of credit at 15% APR. You draw $30,000 to purchase inventory. You'll pay interest only on that $30,000 (roughly $375/month at 15% APR). As you repay the principal, your available credit increases back toward $100,000.

Types of Business Lines of Credit

Secured vs Unsecured

- Secured Lines - Backed by collateral (real estate, equipment, inventory, accounts receivable). Offer lower rates and higher limits but risk asset loss if you default.

- Unsecured Lines - No collateral required, but higher rates and stricter qualification requirements. Most online lenders offer unsecured lines.

Revolving vs Non-Revolving

- Revolving - Credit replenishes as you repay. Most business lines of credit are revolving.

- Non-Revolving - Once repaid, the line closes. Functions more like a term loan with flexible draws.

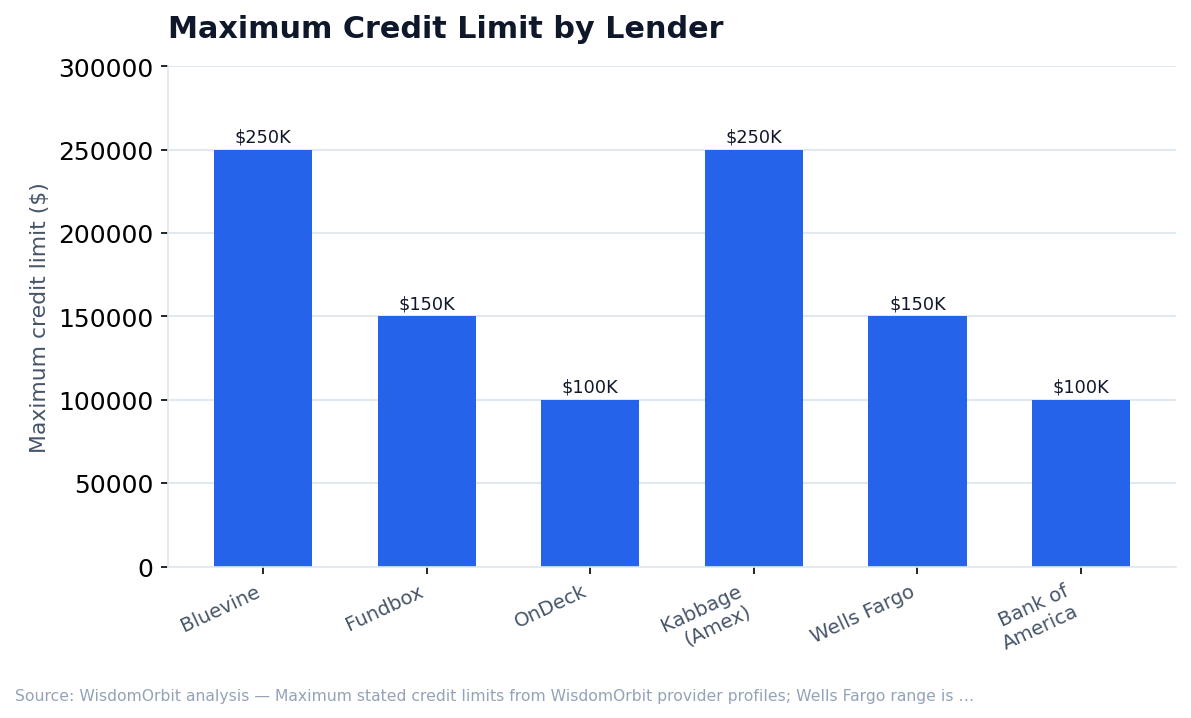

Top Business Line of Credit Providers

Bluevine

Bluevine offers lines of credit up to $250,000 with rates starting at 6.2%. They're known for fast approval (often within minutes) and no origination fees. Requirements include 6+ months in business, $10,000+ monthly revenue, and a 625+ credit score. Payments are made weekly via automatic ACH.

Best for: Growing businesses wanting competitive rates and fast funding.

Fundbox

Fundbox provides lines of credit up to $150,000 with 12 or 24-week repayment terms. Their standout feature is simplified qualification - they connect to your accounting software or bank account to assess eligibility algorithmically. Rates start around 4.66% for 12-week terms.

Best for: Businesses wanting quick, algorithm-based approval with shorter terms.

OnDeck

OnDeck offers lines of credit up to $100,000 with 12-month terms. They can fund same-day in some cases and have a strong track record serving small businesses. Rates range from 29.9% to 56.5% APR (total cost includes fees). Requirements: 1+ year in business, $100,000+ annual revenue.

Best for: Established businesses needing fast access to capital.

American Express Business Line of Credit (formerly Kabbage)

Formerly known as Kabbage before its acquisition, the American Express Business Line of Credit offers automated lines of credit up to $250,000 with 6, 12, or 18-month terms. The application connects to your business bank account, accounting software, or e-commerce platforms for instant decisions. Monthly fees range from 1.25% to 10% of the borrowed amount.

Best for: E-commerce businesses and those wanting automated, data-driven approval.

Wells Fargo Business Line of Credit

Wells Fargo offers traditional bank lines of credit from $5,000 to $150,000 for established businesses. Rates are typically prime + margin, making them more competitive than online lenders. Requirements are stricter: 2+ years in business, strong revenue, and good personal credit.

Best for: Established businesses with strong financials wanting the lowest rates.

Bank of America Business Advantage Line of Credit

Bank of America offers lines up to $100,000 with interest-only payments during the draw period. Existing BofA customers may qualify for better terms through Preferred Rewards. Traditional bank underwriting means slower approval but competitive rates.

Best for: Existing Bank of America customers with established businesses.

Line of Credit vs Term Loan vs Business Credit Card

Understanding when to use each financing option:

- Line of Credit - Best for ongoing or unpredictable expenses, cash flow management, and situations where you're unsure how much you'll need. Flexibility is the key advantage.

- Term Loan - Better for one-time, large expenses with known costs (equipment purchase, expansion project). Fixed payments make budgeting predictable.

- Business Credit Card - Good for smaller, frequent expenses. Often has higher rates than lines of credit but may offer rewards. Better for expenses under $10,000.

Common Uses for Business Lines of Credit

- Cash Flow Management - Bridge gaps between paying expenses and receiving customer payments

- Inventory Purchases - Stock up for busy seasons without depleting cash reserves

- Emergency Expenses - Cover unexpected repairs, replacements, or opportunities

- Payroll - Ensure employees are paid on time during slow periods

- Opportunity Costs - Take advantage of vendor discounts or time-sensitive deals

- Marketing Campaigns - Fund advertising when you need to scale quickly

Qualification Requirements

Requirements vary by lender type:

Online Lenders (More Accessible)

- Time in Business - 6 months to 1 year minimum

- Annual Revenue - $50,000 to $100,000 minimum

- Credit Score - 550 to 650+ (varies by lender)

- Bank Account - Active business checking account

Traditional Banks (Stricter Requirements)

- Time in Business - 2+ years typically required

- Annual Revenue - $100,000+ often required

- Credit Score - 680+ personal credit score

- Financial Statements - Tax returns, profit & loss statements, balance sheets

- Collateral - May require for larger lines

Interest Rates and Fees

Total cost depends on your lender and qualifications:

- Bank Lines of Credit - 7% to 15% APR, often prime rate + margin

- Online Lenders - 15% to 80% APR depending on term length and risk profile

- SBA Lines of Credit - Prime + 2.25% to 4.75% for SBA CAPLines program

- Secured Lines - Generally 2-5% lower than unsecured options

Common Fees to Watch

- Origination Fee - 0% to 2% of credit limit

- Draw Fee - Some lenders charge per withdrawal

- Maintenance Fee - Monthly or annual fee to keep line open

- Inactivity Fee - Charged if you don't use the line

Pros and Cons

Advantages

- Flexibility - Borrow only what you need, when you need it

- Cost Efficiency - Pay interest only on borrowed amounts

- Reusable - Credit replenishes as you repay

- Safety Net - Available capital for emergencies without applying for new loans

- Build Business Credit - Responsible use improves your credit profile

Disadvantages

- Variable Rates - Interest rates may increase over time

- Temptation to Overborrow - Easy access can lead to unnecessary debt

- Fees - Maintenance and draw fees add to costs

- Lower Limits - Generally smaller amounts than term loans

Frequently Asked Questions

How fast can I get funded?

Online lenders often fund within 24-48 hours after approval. Traditional banks may take 1-2 weeks for underwriting and funding.

Will applying hurt my credit score?

Most lenders do a soft pull for pre-qualification (no impact). A hard pull occurs when you formally apply, which may temporarily lower your score by a few points.

Can I pay off my line of credit early?

Yes, most lines of credit have no prepayment penalties. Paying early saves on interest charges.

What happens if I don't use my line of credit?

Some lenders charge inactivity fees. Others may close unused lines after 12-24 months. Check your terms to understand any non-use consequences.

How to Apply

- Check Your Credit - Know your personal and business credit scores before applying

- Gather Documents - Bank statements, tax returns, business licenses, financial statements

- Compare Options - Get quotes from multiple lenders to compare rates and terms

- Apply - Start with online pre-qualification to avoid hard credit pulls until you're ready

- Review Terms - Understand all fees, repayment schedules, and conditions before accepting

Sources & References

- U.S. Small Business Administration – SBA Loan Programs

- Federal Reserve Banks – Small Business Credit Survey

- Consumer Financial Protection Bureau – Small business lending resources

- National Small Business Association – Credit access survey data

Related Articles

This article is for general information only and is not financial, legal, or tax advice. Verify current rates, fees, and terms with providers before making decisions.