Key Takeaways

- The best personal loans in 2026 start at 6.99% APR for borrowers with excellent credit — compared to the average credit card APR of 24.62%.

- Loan amounts range from $1,000 to $100,000 depending on the lender, with repayment terms of 2 to 12 years.

- Seven of the ten lenders reviewed charge zero origination fees; three charge fees ranging from 1.85% to 10%.

- Most lenders offer pre-qualification with a soft credit check, so you can compare rates without impacting your credit score.

- Borrowers who consolidate $20,000 in credit card debt (at 24% APR) into a personal loan at 10% APR save approximately $6,100 in interest over a five-year term.

What Is a Personal Loan?

A personal loan is a fixed-amount, fixed-rate installment loan that you repay in equal monthly payments over a set period. Unlike a mortgage or auto loan, personal loans are typically unsecured — meaning they do not require collateral. Lenders approve you based on your credit score, income, employment history, and debt-to-income ratio (DTI).

Personal loans are one of the most versatile financial products available. You can use them for virtually any legal purpose: consolidating high-interest debt, financing home improvements, covering medical expenses, funding a wedding, or handling an unexpected emergency. The fixed interest rate and predictable monthly payment make budgeting straightforward compared to revolving credit like credit cards.

According to TransUnion, Americans held approximately $245 billion in personal loan balances as of Q4 2025, up 7% year-over-year. The average personal loan balance was $11,281, and the average interest rate was 12.35% APR. Demand continues to grow as consumers recognize the cost advantage over credit card debt.

The 2026 Personal Loan Rate Environment

Personal loan rates are influenced by the Federal Reserve’s federal funds rate, which sits at 3.50%–3.75% as of June 2026 (bank prime rate 6.75%, per the Federal Reserve’s H.15 release). After aggressive rate hikes in 2022–2023, the Fed began easing in late 2024, and rates have stabilized.

For borrowers, this environment means personal loan APRs remain elevated compared to the near-zero rate era of 2020–2021, but have come down from their 2023 peaks. The best-qualified borrowers (credit scores of 720 or higher) can find rates starting at 6.99% to 8.99% APR. Borrowers in the 670–719 range typically see offers between 10% and 16% APR. Those with fair credit (580–669) may face rates of 18% to 30% APR.

Even at these levels, personal loans remain significantly cheaper than credit cards. The Federal Reserve’s latest data shows the average credit card interest rate reached 24.62% APR in Q1 2026, making debt consolidation via a personal loan an attractive strategy for many households.

Best Personal Loans of 2026: Full Comparison

We evaluated ten personal loan lenders across the metrics that matter most to borrowers: APR range, loan amounts, repayment terms, origination fees, funding speed, and minimum credit score requirements. Here is a side-by-side comparison.

APR ranges are indicative and reflect rates for qualified borrowers; lenders reprice frequently, so confirm current rates on each lender’s site. Your actual rate may vary based on creditworthiness, loan amount, and term length. Rates are subject to change.

In-Depth Reviews: Top 10 Personal Loan Lenders

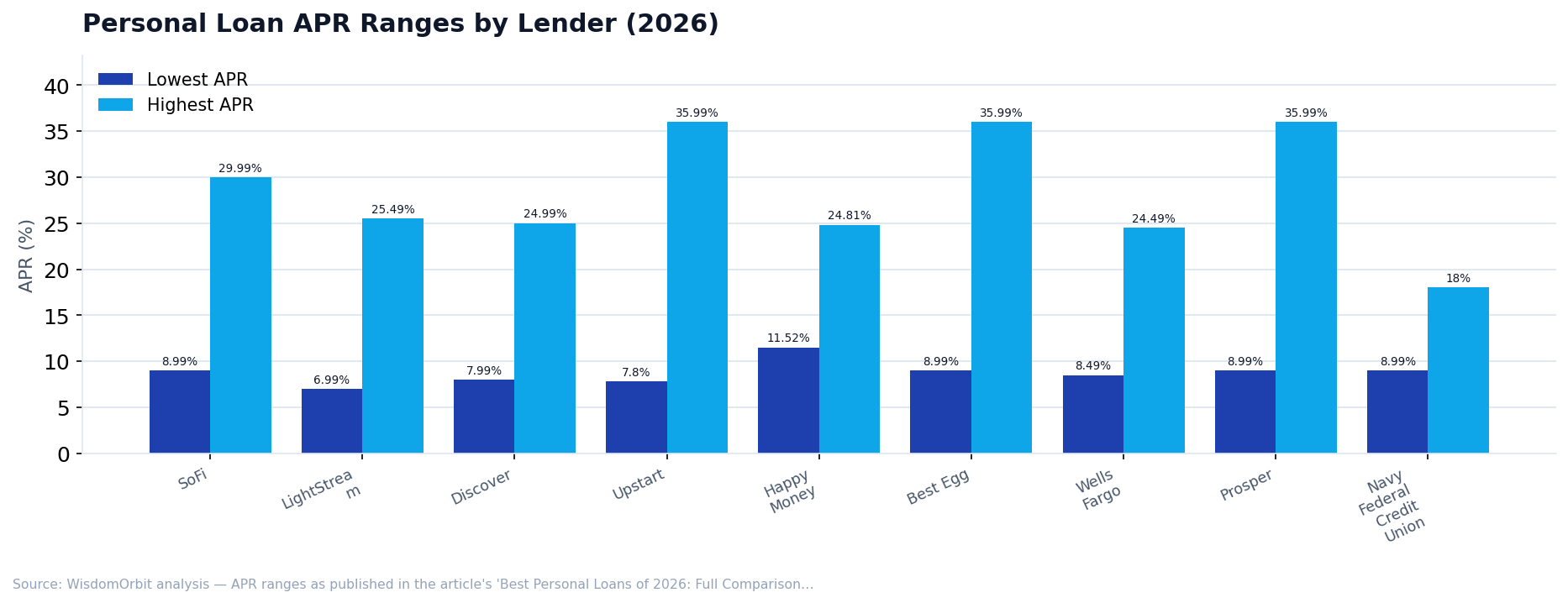

1. SoFi — Best Overall Personal Loan

SoFi has built one of the most comprehensive personal loan products in the market. With APRs starting at 8.99% and loan amounts up to $100,000, SoFi covers everything from modest debt consolidation to major expenses like home renovations or medical procedures.

What sets SoFi apart is its no-fee structure. There are no origination fees, no late fees, and no prepayment penalties. SoFi also offers unemployment protection: if you lose your job, the lender will temporarily pause your payments and help you find new employment through its career services program.

SoFi members get access to financial planning sessions, rate discounts through autopay (typically 0.25% off), and the broader SoFi ecosystem of investing, banking, and insurance products. Same-day funding is available for many borrowers.

Pros: No fees whatsoever; unemployment protection; large loan amounts up to $100K; same-day funding available; member benefits (financial planning, career services).

Cons: Requires good credit (minimum ~680); joint applications not accepted; no option for secured loans.

2. LightStream — Best for Excellent Credit

LightStream, a division of Truist Bank (formerly SunTrust), offers some of the lowest personal loan rates in the industry. If you have excellent credit (720+), a stable income, and a strong borrowing history, LightStream’s starting APR of 6.99% is hard to beat.

LightStream’s Rate Beat Program is unique: if you receive a lower rate from another lender for the same loan terms, LightStream will beat it by 0.10 percentage points (subject to terms). The lender also offers extended terms up to 12 years for larger loans, reducing monthly payments.

The trade-off is that LightStream has higher qualification standards than most competitors. There is no pre-qualification tool — applying triggers a hard credit inquiry immediately. The minimum loan amount of $5,000 also rules out borrowers who need smaller sums.

Pros: Industry-leading low APRs; no fees; terms up to 12 years; Rate Beat Program; same-day funding.

Cons: No pre-qualification (hard inquiry only); high credit requirements; $5K minimum loan; no direct pay for debt consolidation.

3. Marcus by Goldman Sachs — No Longer Accepting New Applications

Update (June 2026): Goldman Sachs wound down its consumer-lending business, and Marcus no longer accepts new personal-loan applications. Existing loans continue to be serviced; the details below are retained for reference only.

Marcus offers a clean, transparent personal loan with zero fees and a unique due-date flexibility feature. Borrowers who make 12 consecutive on-time payments can defer one monthly payment (interest still accrues), providing a useful safety net during tight months.

Marcus loans range from $3,500 to $40,000 with terms of 3 to 6 years. The APR range of 8.99% to 29.99% is competitive for borrowers with good credit. Marcus also offers pre-qualification through a soft credit check, so you can see your rate without any impact on your score.

The backing of Goldman Sachs provides institutional credibility, and the application process is entirely online. Funding typically occurs within 1 to 4 business days of approval.

Pros: Zero fees; due-date flexibility after 12 payments; soft pre-qualification; Goldman Sachs backing.

Cons: Maximum loan of $40K; no joint applications; slower funding than SoFi or LightStream; no mobile app for loan management.

4. Discover Personal Loans — Best for Debt Consolidation

Discover stands out for its direct-pay feature: when you take a debt consolidation loan, Discover can send funds directly to your creditors on your behalf. This removes the temptation to spend the loan proceeds and ensures your existing debts are paid off cleanly.

With APRs from 7.99% to 24.99% and no origination fees, Discover offers competitive pricing. The minimum loan of $2,500 makes it accessible for smaller consolidation needs. Discover also has a strong customer service reputation, consistently ranking high in J.D. Power customer satisfaction surveys.

Pros: Direct-pay to creditors; no fees; strong customer service; low minimum loan amount.

Cons: Funding takes 1 to 7 days; minimum credit score ~660; maximum loan of $40K.

5. Upstart — Best for Fair or Limited Credit

Upstart uses an AI-driven underwriting model that evaluates factors beyond traditional credit scores, including education, work history, and income trajectory. This makes Upstart the strongest option for younger borrowers, recent graduates, or anyone with a thin credit file who might be denied by traditional lenders.

Upstart’s APR range is wide (7.80%–35.99%), reflecting the broader risk profile of its borrower base. Origination fees of 0% to 10% also apply depending on your risk level. The minimum credit score is just 300, and borrowers with scores as low as 580 regularly receive funding.

According to Upstart’s published data, 84% of approved loans are fully automated with no human intervention, and most borrowers receive funds by the next business day.

Pros: AI-driven approval; accepts thin credit files; very low minimum credit score; fast automated process.

Cons: Origination fees up to 10%; high max APR of 35.99%; maximum loan of $50K; shorter terms (3–5 years).

6. Happy Money — Best for Credit Card Payoff

Happy Money (formerly Payoff) is the only lender on this list that exclusively funds credit card payoff loans. If your goal is specifically to eliminate credit card debt, Happy Money’s focused approach has advantages: the lender sends funds directly to your credit card issuers, and its tools are designed around the psychological aspects of debt elimination.

APRs range from 11.52% to 24.81%, with origination fees of 1.85% to 5.99%. While not the cheapest option, Happy Money is a good fit for borrowers who need structure and accountability to get out of credit card debt.

Pros: Direct payoff to credit card issuers; focused debt-elimination tools; soft pre-qualification.

Cons: Credit card payoff only; origination fees; higher starting APR; limited use flexibility.

7. Best Egg — Best for Fast Funding

Best Egg is known for speed. Many borrowers receive funds as soon as the next business day after approval, and the online application takes just minutes. Loan amounts range from $2,000 to $50,000, making Best Egg suitable for a wide variety of needs.

The downside is origination fees ranging from 0.99% to 8.99%, which are deducted from your loan proceeds. On a $10,000 loan with a 5% origination fee, you would receive $9,500 while repaying $10,000 plus interest. Factor this into your cost comparison.

Pros: Fast funding (often next day); low minimum loan; flexible use; simple online process.

Cons: Origination fees up to 8.99%; high max APR of 35.99%; shorter terms (3–5 years).

8. Wells Fargo — Best for Existing Customers

Wells Fargo offers competitive personal loan rates, especially for existing banking customers who benefit from relationship discounts. The APR range of 8.49% to 24.49% is solid, and loan amounts up to $100,000 are available for qualified borrowers.

The key advantage is integration with Wells Fargo’s banking ecosystem. If you already have a Wells Fargo checking or savings account, managing your loan alongside your other finances is seamless. The bank also offers terms starting at just 12 months for smaller, short-term needs.

Pros: Large loan amounts up to $100K; relationship discounts; flexible terms starting at 1 year; established bank with branch access.

Cons: Best rates require existing Wells Fargo relationship; slower online experience vs. fintech lenders; no pre-qualification tool.

9. Prosper — Best Peer-to-Peer Lending Option

Prosper is one of the original peer-to-peer lending platforms. Instead of funding loans from its own balance sheet, Prosper connects borrowers with individual and institutional investors. This model can benefit borrowers who may not qualify with traditional lenders.

APRs range from 8.99% to 35.99%, with origination fees of 2.41% to 5%. Prosper accepts borrowers with credit scores as low as 600, though rates at that level will be steep. Checking your rate requires only a soft credit inquiry.

Pros: Peer-to-peer model; accepts lower credit scores; soft pre-qualification; joint applications available.

Cons: Origination fees always apply; funding takes 3–5 business days (investor matching); high rates for lower credit scores.

10. Navy Federal Credit Union — Best for Military Members

Navy Federal Credit Union offers personal loans exclusively to military members, veterans, and their families. The APR cap of 18.00% is a major advantage — many lenders have max APRs above 30%. Combined with no origination fees and loan amounts starting at just $250, Navy Federal is exceptionally accessible.

Membership is required (open to active-duty military, veterans, DoD civilians, and their family members). If you qualify, Navy Federal’s personal loan is one of the most borrower-friendly options available. Check our VA home loans guide for other military-specific financial products.

Pros: Low max APR of 18%; no fees; very low minimums ($250); military-friendly.

Cons: Membership required (military/DoD/family only); shorter max term of 5 years; in-branch application may be needed for larger amounts.

How to Choose the Right Personal Loan

Choosing the right personal loan is not just about finding the lowest APR. Consider these five factors in order of importance:

1. Total Cost of the Loan (APR + Fees)

APR tells part of the story, but origination fees can significantly increase your total cost. A loan at 9% APR with a 5% origination fee may cost more than a loan at 10% APR with no fees, depending on the term length. Always calculate the total interest paid plus any fees to compare true costs.

Here is a worked example: Borrowing $15,000 over 5 years at 10% APR with no fees results in total interest of approximately $4,146 and total payments of $19,146. The same loan at 9% APR with a 5% origination fee means you receive $14,250 (after the $750 fee is deducted) but repay $15,000 plus approximately $3,713 in interest, for a total cost of $18,713 — but you only got $14,250 in hand. Your effective total cost is $4,463 on the money you actually received.

2. Monthly Payment Affordability

Longer terms reduce your monthly payment but increase total interest paid. Use this general guideline: keep your total monthly debt payments (including the new personal loan) below 36% of your gross monthly income. This is the debt-to-income ratio most lenders use as a threshold.

3. Funding Speed

If you need money urgently — for a medical bill, car repair, or time-sensitive opportunity — lenders like SoFi and LightStream can fund same-day. Prosper’s peer-to-peer model takes 3 to 5 days. Traditional banks may take a week or more.

4. Lender Reputation and Support

Check customer satisfaction ratings, Better Business Bureau (BBB) ratings, and CFPB complaint data. Discover, SoFi, and Navy Federal consistently rank among the highest-rated lenders. Read reviews specifically about the loan servicing experience, not just the application process.

5. Borrower Benefits

Some lenders offer features that add genuine value: SoFi’s unemployment protection, Marcus’s payment deferral, LightStream’s Rate Beat Program, and Discover’s direct-pay to creditors. These can make a meaningful difference over the life of your loan.

Personal Loans vs. Other Borrowing Options

A personal loan is not always the right choice. Here is how it compares to other common borrowing options:

When a personal loan is the right choice: You need $2,000 or more, want a fixed rate and predictable monthly payment, plan to repay over 2 to 7 years, and prefer not to put up collateral. Personal loans are especially advantageous for consolidating credit card debt, where the APR savings alone can justify the loan.

When to consider alternatives: If you can pay off debt within 12–18 months, a 0% balance transfer card may cost less. If you own a home and need $50,000+, a home equity loan typically offers lower rates (though with the risk of your home as collateral). For business purposes, an SBA loan or business line of credit is usually more appropriate than a personal loan.

How to Apply for a Personal Loan: Step-by-Step

The application process is straightforward, but preparation makes a significant difference in the rate you receive.

Step 1: Check Your Credit Score

Before applying, know your credit score. You can check it for free at AnnualCreditReport.com (full credit report) or through most banking apps (credit score). If your score is below 670, consider spending 3 to 6 months improving it before applying — even a 30-point increase can drop your APR by 2 to 4 percentage points, saving hundreds or thousands over the life of the loan.

Step 2: Pre-Qualify With Multiple Lenders

Most lenders (except LightStream) offer pre-qualification through a soft credit inquiry, which does not affect your score. Pre-qualify with at least three to five lenders to compare actual rate offers. The advertised “starting from” rate applies to very few borrowers — your actual offer may be higher.

Step 3: Compare Total Costs

For each offer, calculate the total repayment amount: principal + total interest + origination fees. Do not just compare APRs in isolation. Use an online personal loan calculator or ask each lender for a full amortization schedule.

Step 4: Gather Documentation

Most lenders require: government-issued ID, proof of income (recent pay stubs or tax returns), proof of address, Social Security number, and bank account information for funding. Self-employed borrowers may need additional documentation like profit-and-loss statements or two years of tax returns.

Step 5: Submit Your Application

Choose the lender with the best total cost and formally apply. This triggers a hard credit inquiry. Once approved, review the final terms carefully — ensure the APR, loan amount, term, and monthly payment match what was quoted during pre-qualification. Sign the agreement and receive your funds.

How Personal Loans Affect Your Credit Score

Taking a personal loan creates both positive and temporary negative effects on your credit score. Understanding these dynamics helps you make an informed decision.

Temporary negative impact: The hard credit inquiry from your application can lower your score by 5 to 10 points. A new account also reduces your average age of credit. These effects are minor and typically recover within 3 to 6 months.

Positive long-term impact: A personal loan adds an installment account to your credit mix, which can boost your score if your profile was previously dominated by revolving credit (credit cards). If you use the loan to pay off credit card balances, your credit utilization ratio drops — often dramatically — which is the single largest factor in credit score improvement after payment history.

According to FICO, payment history accounts for 35% of your score, and credit utilization accounts for 30%. A borrower who consolidates $15,000 in credit card debt (reducing utilization from 75% to near 0%) and makes on-time personal loan payments for 12 months could see their credit score increase by 50 to 100+ points.

Common Personal Loan Mistakes to Avoid

In our analysis of personal loan outcomes, these are the most costly mistakes borrowers make:

- Only comparing APR, not total cost. A lower APR with a high origination fee can cost more than a slightly higher APR with no fee. Always compare total repayment amounts.

- Borrowing more than you need. It is tempting to take the maximum offered, but every extra dollar you borrow costs interest. Borrow only what you need for your specific purpose.

- Choosing the longest term for the lowest payment. A 7-year term cuts your monthly payment but nearly doubles the total interest compared to a 3-year term. Choose the shortest term you can comfortably afford.

- Not pre-qualifying with multiple lenders. Rate offers vary significantly between lenders, even for borrowers with the same credit profile. Shopping around can save 2 to 5 percentage points on your APR.

- Using a debt consolidation loan, then running up credit card balances again. This is the most expensive mistake. If you consolidate $20,000 in credit card debt but then accumulate $15,000 in new charges, you now owe $35,000. Close or freeze the paid-off cards to remove the temptation.

- Ignoring the fine print on fees. Some lenders charge late fees ($15–$39 per occurrence), returned payment fees, or even check-processing fees. Read the loan agreement thoroughly before signing.

Frequently Asked Questions

What credit score do I need for a personal loan?

Most lenders require a minimum credit score of 580 to 660 for personal loan approval. However, the best rates (under 10% APR) are typically reserved for borrowers with good to excellent credit scores of 670 or above. Some lenders like Upstart use alternative data beyond credit scores, making approval possible for borrowers with limited credit history.

Does applying for a personal loan hurt my credit score?

Pre-qualification (soft inquiry) does not affect your credit score, and most lenders now offer this option. A hard inquiry occurs only when you formally apply and can temporarily lower your score by 5 to 10 points. Once you receive the loan, making on-time payments can actually improve your credit score over time by adding positive payment history and improving your credit mix.

How long does it take to get a personal loan?

Many online lenders can approve applications within minutes and fund loans as fast as the same business day or next business day. Traditional banks and credit unions may take 2 to 7 business days for approval and an additional 1 to 3 days for funding. SoFi and LightStream are known for same-day funding in many cases.

Can I use a personal loan to pay off credit card debt?

Yes, debt consolidation is one of the most common and financially beneficial uses of a personal loan. If your credit card APR is 20% to 28% and you qualify for a personal loan at 8% to 14%, you can save thousands in interest over the repayment period. Some lenders like Happy Money specialize exclusively in credit card payoff loans and will send funds directly to your credit card issuers.

What is the difference between a secured and unsecured personal loan?

An unsecured personal loan requires no collateral and is approved based on your creditworthiness, income, and debt-to-income ratio. Most personal loans are unsecured. A secured personal loan requires collateral such as a savings account, CD, or vehicle, which the lender can seize if you default. Secured loans typically offer lower interest rates because they carry less risk for the lender, but you risk losing the pledged asset.

Editor’s Insight

After analyzing personal loans for over a decade, my strongest recommendation is this: treat a personal loan as a financial tool with a specific purpose, not as free money. The borrowers who benefit most are those who use the loan to eliminate expensive credit card debt and then commit to not accumulating new balances. If you can consolidate $15,000 to $25,000 in credit card debt at half the interest rate, the math is unambiguous — you should do it. But the loan only works if you pair it with behavioral change. Cut up the paid-off cards or freeze them, set up autopay on the personal loan, and build a small emergency fund so you do not need to fall back on credit cards when the unexpected happens.

Sources & References

- TransUnion. “Consumer Credit Origination, Balance and Delinquency Trends — Q4 2025.” transunion.com

- Board of Governors of the Federal Reserve System. “Consumer Credit — G.19.” federalreserve.gov

- Consumer Financial Protection Bureau (CFPB). “What Is a Personal Loan?” consumerfinance.gov

- FICO. “What’s in My FICO Scores?” myfico.com

- Federal Reserve Bank of New York. “Quarterly Report on Household Debt and Credit.” newyorkfed.org

- Bankrate. “Average Credit Card Interest Rates.” bankrate.com